LazingBee/iStock via Getty Images

LazingBee/iStock via Getty Images

(Note: This report was published to Beating The Market on 18th March 2022. At the time of writing, the stock was trading at less than $2, and despite its big move (+18.92%) on Friday, it is still in deep value territory.)

Shift (NASDAQ:SFT) is now trading at ~$2.5 per share ($225M in market cap), which is roughly 1.8x the net cash on its balance sheet. It is fair to say that the market is pricing Shift for bankruptcy. We discussed Shift’s cash burn situation (bankruptcy risk) in great detail after the Q3 report, and you can find the discussion here.

For those wondering why Shift is one of my favorite moonshot bets, I urge you to read my investment thesis shared in this note. Although Shift is risky, it is a rare, viable ~100x opportunity. Today, we will briefly skim over Shift’s quarter and spend most of our time on understanding Shift’s path to profitability (shared by management in Q4 investor presentation). Let’s begin.

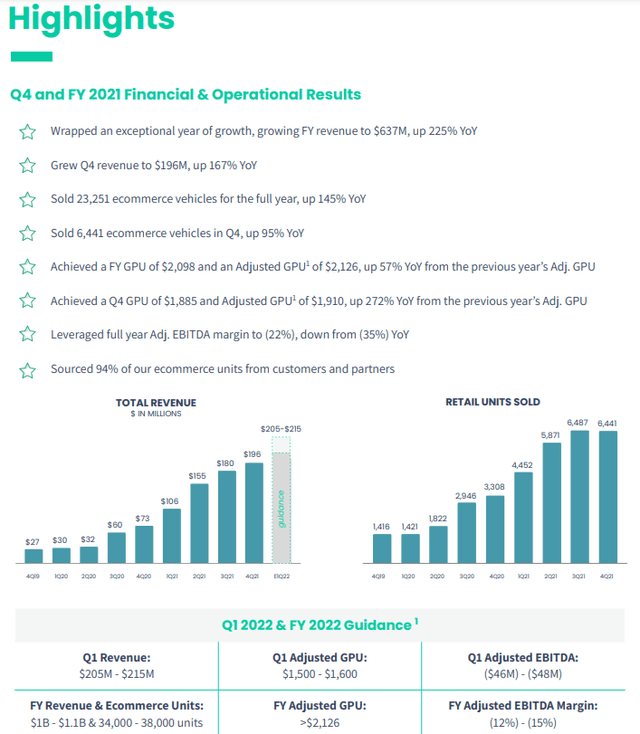

With continued supply chain pressures inducing inflation, the pricing environment in the used-car industry remained robust in Q4 2021. On the back of this strength, Shift generated record revenues of ~$195M (up 167% y/y) in the last quarter, and we are almost through Q1 2022, so the company’s gui de of $205-215M is really actual numbers. In my view, Shift is performing well, and its share price action is absolutely ridiculous.

de of $205-215M is really actual numbers. In my view, Shift is performing well, and its share price action is absolutely ridiculous.

Shift Q4 2021 Shareholder Letter

In addition to strong unit sales, Shift’s gross profit per unit was robust in Q4 (considering seasonal weakness). For Q1 2022, Shift’s adj. GPU guidance of $1500-1600 may seem weak, but this is just a result of price rise normalization in the used-car industry (and seasonality). The attach rate for ancillary services is improving, and as such, Shift expects to record adj. GPUs of 2200+ in this year. In my opinion, the top-end of revenue and unit guidance of $1.1B and 38,000 units is conservative and sets up the company for a series of “beats and raises” in 2022. Overall, Shift’s Q4 was in-line with our expectations from the company, and I am happy with the reported numbers.

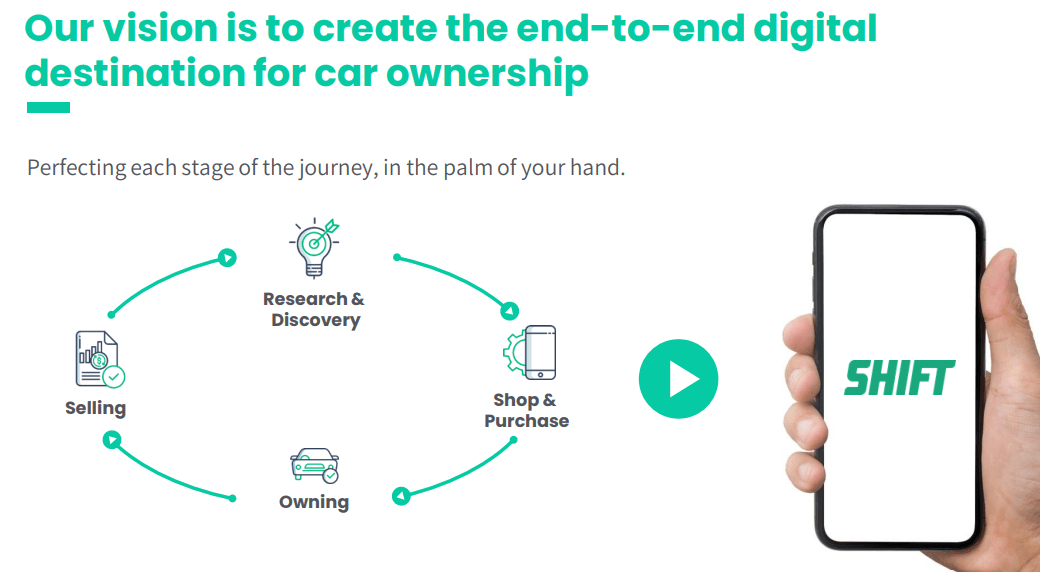

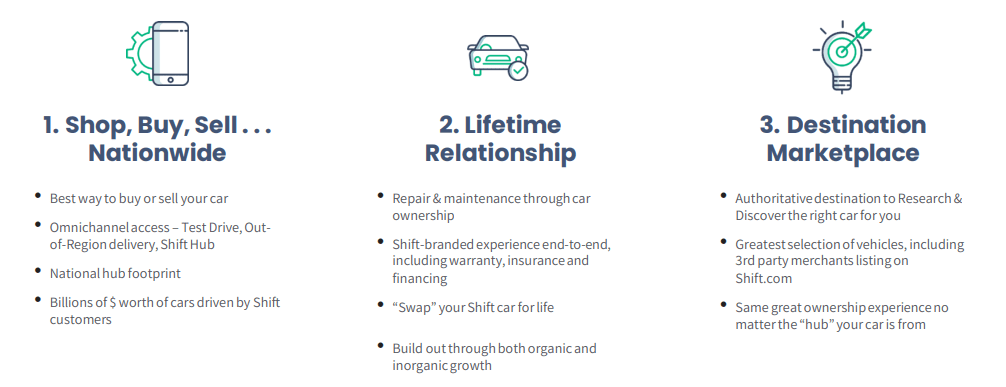

As Shift continues to scale revenue, it is delivering operating leverage as evidenced by narrowing (highly negative) EBITDA margins. For 2021, Shift’s adj. EBITDA margin came in at -22% vs. -37% (figure from 2020). In 2022, Shift’s management expects this margin profile to improve significantly from -22% to a range of -12% to -15%. While Shift is years away from breakeven (and FCF generation), the business is scaling up rapidly and simultaneously improving operational efficiencies. After undergoing some managerial upheaval in the last few quarters, the company seems to have settled on the executive leadership team of George Arison [co-founder, CEO], Oded Shein [CFO], and Jeff Clementz [President] – people with experience of growing e-commerce businesses. Along with Q4 results, Shift’s management released an investor presentation that outlined Shift’s path to EBITDA breakeven.

Shift Q4 2021 Shareholder Letter

In addition to strong unit sales, Shift’s gross profit per unit was robust in Q4 (considering seasonal weakness). For Q1 2022, Shift’s adj. GPU guidance of $1500-1600 may seem weak, but this is just a result of price rise normalization in the used-car industry (and seasonality). The attach rate for ancillary services is improving, and as such, Shift expects to record adj. GPUs of 2200+ in this year. In my opinion, the top-end of revenue and unit guidance of $1.1B and 38,000 units is conservative and sets up the company for a series of “beats and raises” in 2022. Overall, Shift’s Q4 was in-line with our expectations from the company, and I am happy with the reported numbers.

As Shift continues to scale revenue, it is delivering operating leverage as evidenced by narrowing (highly negative) EBITDA margins. For 2021, Shift’s adj. EBITDA margin came in at -22% vs. -37% (figure from 2020). In 2022, Shift’s management expects this margin profile to improve significantly from -22% to a range of -12% to -15%. While Shift is years away from breakeven (and FCF generation), the business is scaling up rapidly and simultaneously improving operational efficiencies. After undergoing some managerial upheaval in the last few quarters, the company seems to have settled on the executive leadership team of George Arison [co-founder, CEO], Oded Shein [CFO], and Jeff Clementz [President] – people with experience of growing e-commerce businesses. Along with Q4 results, Shift’s management released an investor presentation that outlined Shift’s path to EBITDA breakeven.

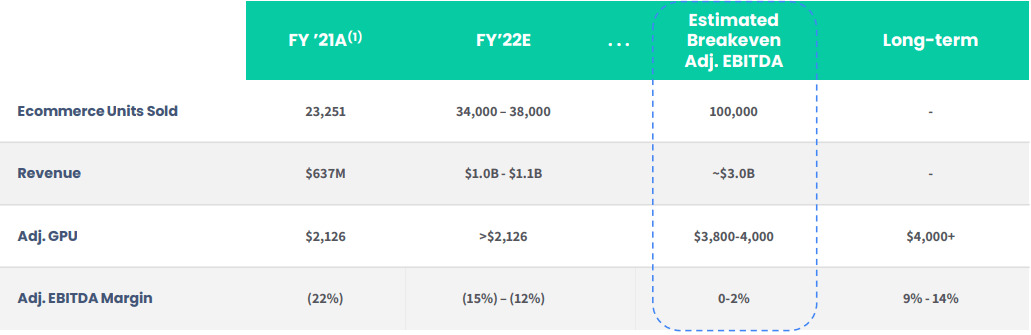

Let’s study this multi-year plan and its feasibility.

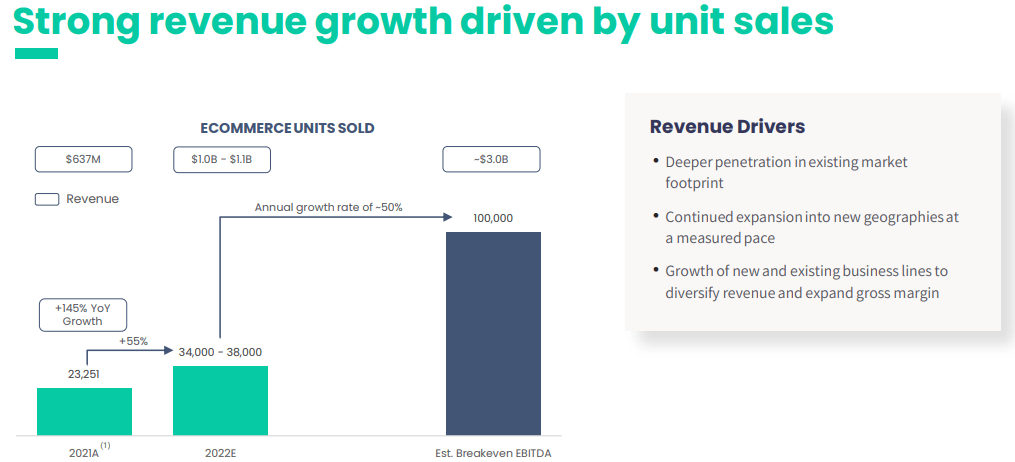

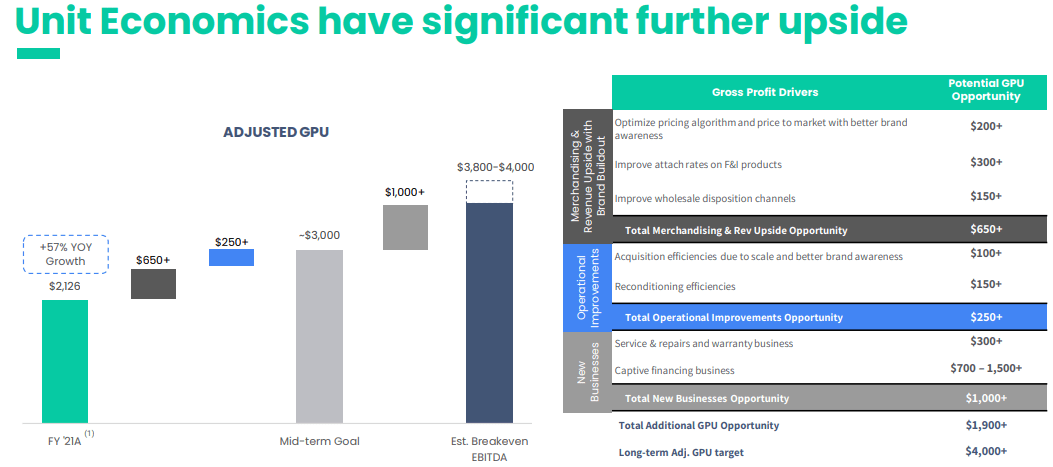

According to Shift’s management, the company could achieve EBITDA breakeven on an adjusted-basis at annual revenues of $3B (100,000 e-commerce unit sales) with adj. GPU reaching the $3800 to $4000 range. To achieve these figures, Shift needs 3-4 years of 50%+ sales growth and consistent improvement in margin profile.

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

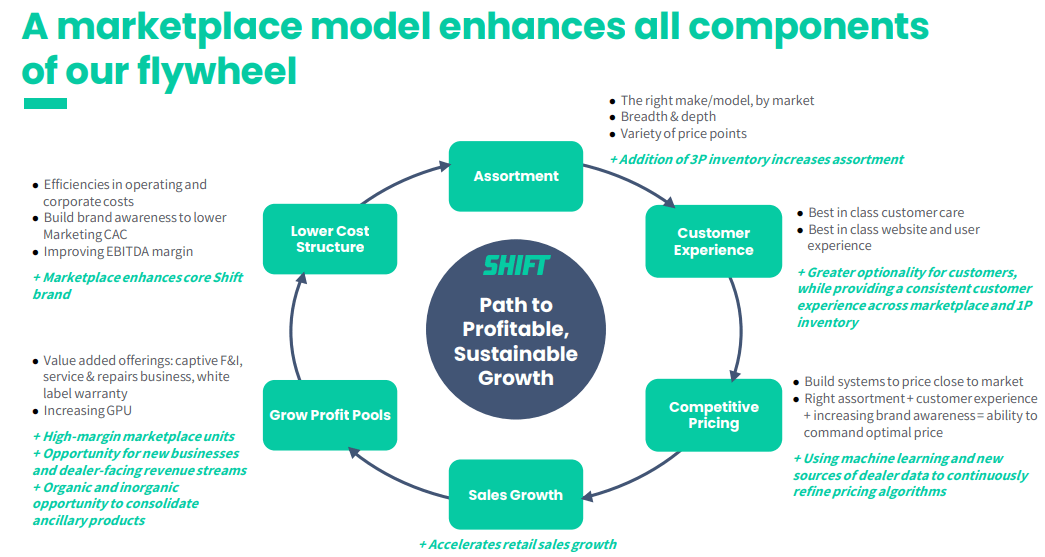

Shift’s EBITDA breakeven model is based on scale, innovation (ancillary products and services), and operational efficiencies. Over the next 3-4 years, Shift is projecting unit sales to grow at an annualized rate of 50%+. Looking at Carvana’s growth trajectory, I think these projections are highly conservative. However, Shift’s balance sheet will (more or less) dictate its sales growth, and with only $200M of cash on the balance sheet at the end of 2021, the company will need a cash injection or two to achieve this scale.

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

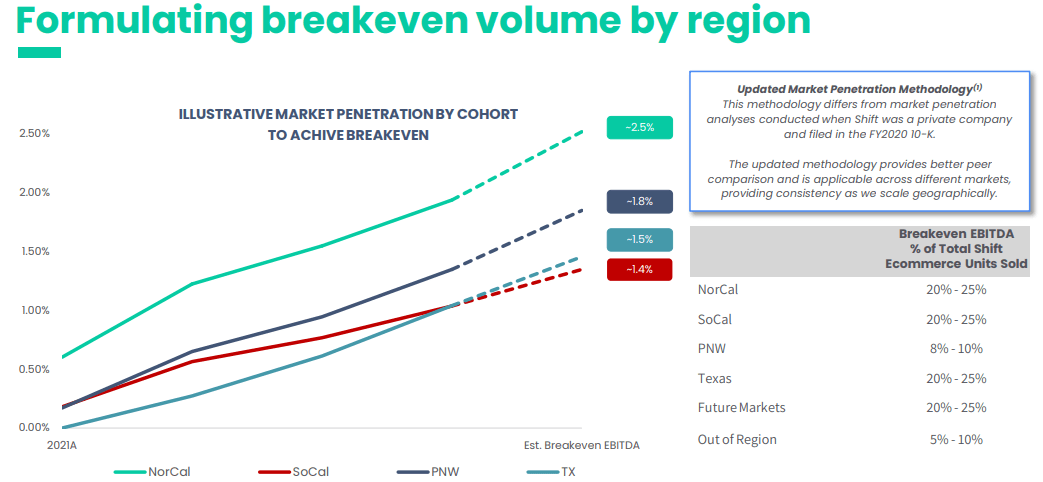

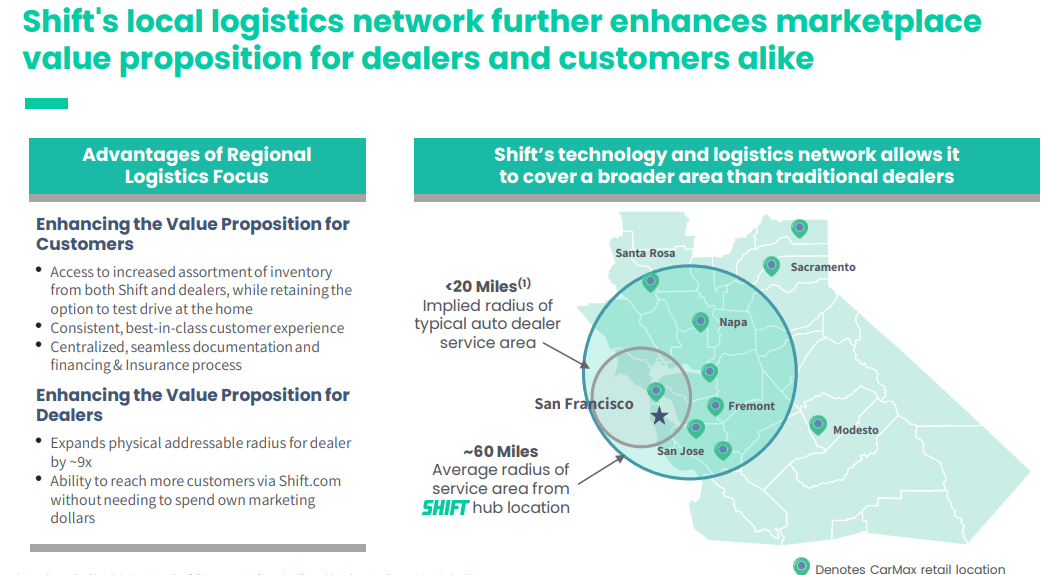

Shift’s sales growth projections are predicated primarily on expansion in existing markets – California and Texas. Shift has already demonstrated its ability to grow its market share to 4%+ in the San Francisco region, and a replication of this playbook in other markets is not very complicated due to used cars (cars in general) being a commodity with few brands and models. Hence, I am convinced of Shift’s ability to gain higher market share and scale up to a level where profitability is achievable. Will Shift get the growth capital required to get there? I think so, but more on it later.

For now, Shift is a cash-burning machine. In 2021, Shift’s adj. GPUs expanded to ~$2100, resulting in positive trends in operating leverage. However, the company is spending a lot more on SG&A than it makes in gross profits, as Shift enters new geographical markets and chases market share in existing markets while attempting to build a national brand.

Can Shift ever become profitable? My take is yes; it can be profitable.

My confidence stems from the significant upside in Shift’s unit economics. With Shift expected to rake in $1.1B in revenue in 2022, it is ready to enter the captive financing business (Shift will finance the loans on its platform and securitize them via ABSs [instead of redirecting customers to bank partners]), which could alone tack on $700-$1500+ in adj. GPU. Shift’s management also sees massive upside in unit economics from optimization of AI/ML pricing models, higher attach rates on F&I products, improvements in wholesale disposition channels, greater brand awareness, and economies of scale in reconditioning, service and repairs.

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

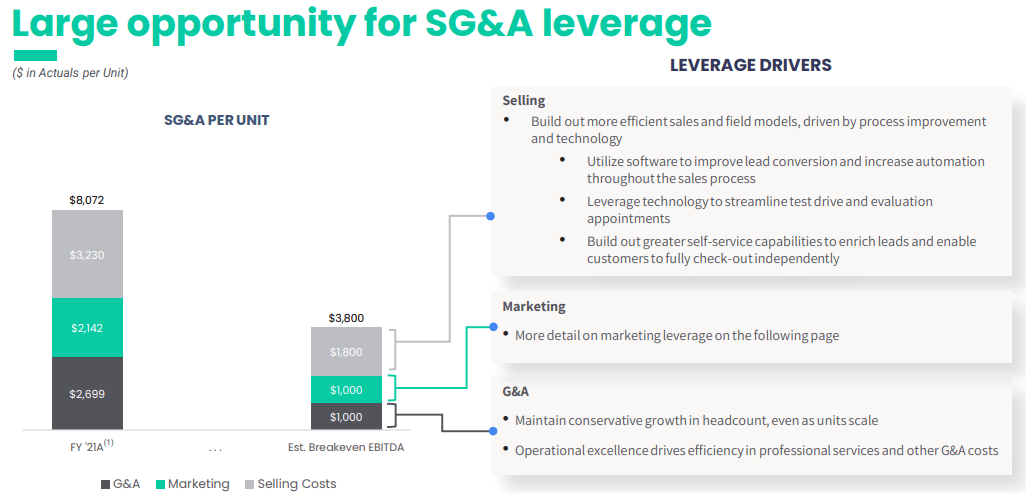

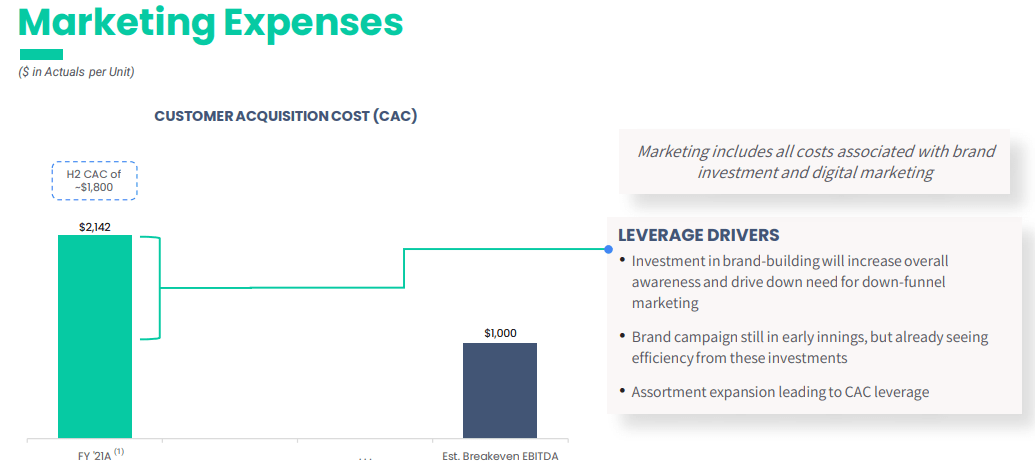

For Shift to achieve breakeven EBITDA, doubling its GPUs won’t be enough. The company will also need to collapse it’s per unit SG&A spending, i.e., drive significant operational efficiencies. In 2021, Shift’s SG&A per unit was $8,072. This means Shift is losing ~$6,000 per unit on a net-net basis. While filing this gap may feel like a daunting task, Shift’s end-to-end ecosystem has ample room for SG&A compression (as a %age of revenues, not dollar amount).

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Considering used-car industry TAM of $840B and low e-commerce penetration (<2%) in this market, scaling up (at 50%+ annualized growth for the next five years) shouldn’t be much of a challenge for Shift. However, improving unit economics (adj. GPU to $3800 to $4000) and compressing SG&A spending are going to be critical to the success of Shift’s medium-term plans outlined above. We will continue to monitor progress on this front over the coming quarters, but I think these numbers are more than achievable over the next 3-4 years.

With a tighter financial environment amid macroeconomic challenges, Shift may find it difficult to get the growth capital (~$400-500M over the next 3-5 years) needed to finance its medium-term growth plans. As a result, the market is betting on bankruptcy for Shift; however, I am taking the contrarian view here. As Shift is trading at net cash value, institutional investors are basically getting the company for free. The interest rate environment is still very much accommodative, and large institutional money can easily bankroll Shift’s path to profitability with cheap debt. And so, I am not at all surprised to learn about Softbank’s investment.

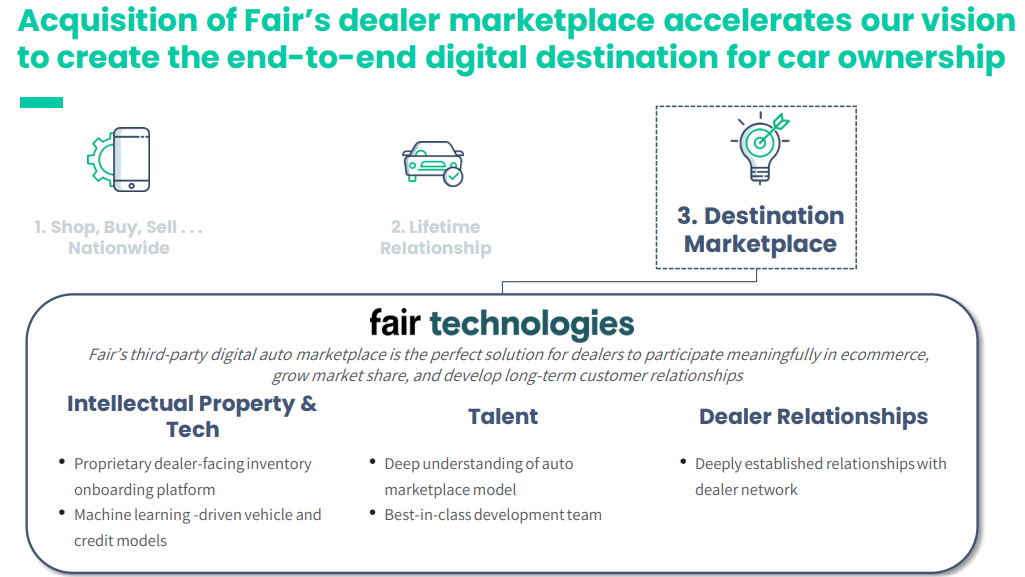

While the market is pricing a bankruptcy for Shift, Softbank Group (one of the largest private equity firms in the world) is investing in Shift’s equity and backing its growth plans with additional debt investments. In my view, Softbank lending money to Shift via unsecured debt at 6% to acquire Fair’s dealer marketplace is a sign of great confidence in Shift’s ability to execute on the medium to long term plan set out by the management team. Although I am not sure about the size of Softbank’s equity investment in Shift, my thinking is that it could be a very sizeable position as Shift’s market cap has been quite depressed in Q4 2021.

Shift’s vision is to become the end-to-end digital destination for car ownership, and in accordance with this vision, Shift is acquiring Fair’s dealer listing marketplace at $15M cash (+2.5% equity of Shift).

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

By adding Fair’s technology to its platform, Shift is strengthening its ecosystem through IP, talent, and dealer relationships. Having a marketplace model in place would considerably increase the inventory available on Shift, which would give customers more options to choose from. Furthermore, this deal enhances Shift’s data capabilities, brand, and profit potential.

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

Now, I do understand that there are hundreds of used-car marketplaces in North America; however, these marketplaces do not have access to proprietary logistics networks like the ones that Shift and other few rivals like Carvana and Vroom possess. Hence, I view the Shift-Fair acquisition deal as a win-win.

Shift Q4 2021 Investor Presentation

Shift Q4 2021 Investor Presentation

With a powerful backer like Softbank, Shift could turn into the ~100x investment that we have touted it as for so long. I have always believed that Shift’s institutional investor base and strategic partners (Lithia Motors) will not let Shift go bankrupt, and management’s confidence in Shift’s ability to attract investors was the highlight of Shift’s Q4 earnings call:

Brian Nagel — Oppenheimer Analyst

How should we think about the funding needs of the business to get to that breakeven point?

Oded Shein — Chief Financial Officer

So we feel very comfortable with our liquidity position at this point. We ended the year with nearly $200 million in the bank. When you think about the growth of the business, we primarily going to fund inventory growth through our floor plan as you’ve heard just signed a new floor plan facility in Q4 that doubled our capacity than before, and we think that can be scaled even higher as we move forward to satisfy inventory growth needs. That being said, we have to think about the future as well.

We feel very good that 2022, we have sufficient liquidity to cover all of our needs. Going forward, we will want to further strengthen our liquidity this year. It can take many different forms. We just issued that.

We can issue additional debt; it could be equity or whatever form that is acceptable to the company and to the market. And then, finally, in the meantime, we’re taking steps to be prudent stewards of cash and we identified means to enhance our cash spend efficiency. So obviously, cash flow is a big focus for us.

George Arison — Co-Chief Executive Officer

Brian, I’ll just add to that that when you look at last year and the excellence in the condition that we saw, coupled with the growth in GPU, both on the front end and the back end, as well as the rapid scaling that we saw last year, and we’ll continue to see this year plus now a very clear path to profitability, it will be all those factors together are the right factors to attract new investors to Shift. We just attracted new investors to Shift with Softbank coming on, both as a debt and an equity investor, and we believe that others will come in the coming quarters as well.

Source: Shift Q4 2021 Earnings Call Transcript

With these new developments (around liquidity and investors) and renewed confidence in Shift’s execution capabilities and leadership team, I am more bullish than I have ever been on the company, and buying it here at net cash (with institutions like Softbank) is an absolute no-brainer. Still, let’s glance over Shift’s valuation before concluding this note.

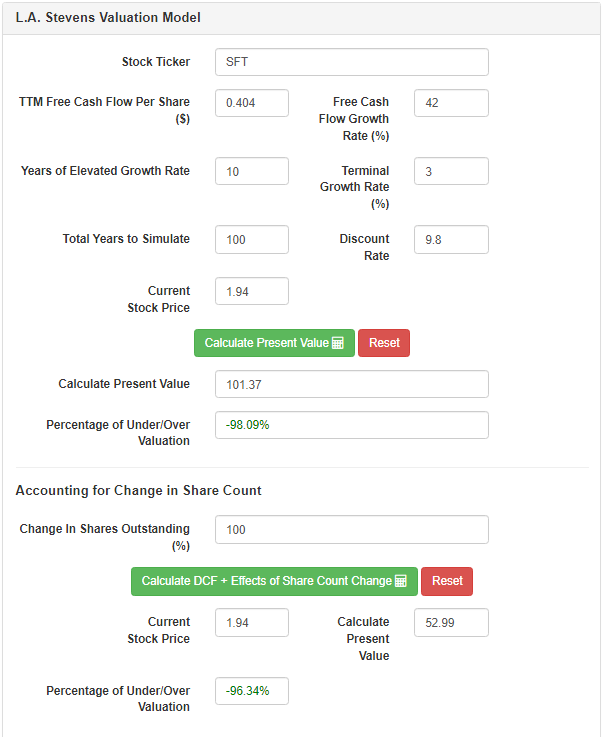

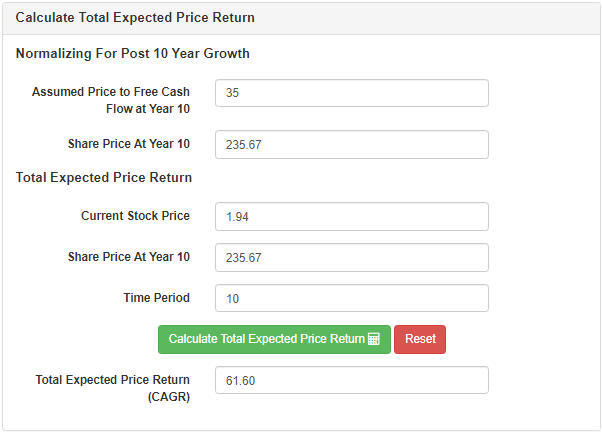

In my view, Shift is a mini-Carvana with room for exponential sales growth. Considering Shift’s TAM of $840B and its 2022 sales guidance of $1.1B, Shift’s growth story is just getting started. In Q4 2021 investor presentation, Shift’s management laid out their path to profitability, and I am convinced these numbers could be achieved within the next four years. At sales growth maturity, Shift should be able to deliver free cash flow margins of 5%-10%. However, to implement a margin of safety, I base my valuation on a 3% potential FCF margin, which is a very conservative estimate for an end-to-end e-commerce business.

2022E revenue [A] (our estimate)

$1.2 billion

Potential Free Cash Flow Margin [B]

3%

Average fully-diluted shares outstanding [C] (including dilution from Fair)

~92 million

Free cash flow per share [ D = (A * B) / C ]

$0.404

Free cash flow per share growth rate

42%

Terminal growth rate

3%

Years of elevated growth

10

Total years to stimulate

100

Discount Rate (Our “Next Best Alternative”)

9.8%

L.A. Stevens Valuation Model

L.A. Stevens Valuation Model

Summary of results:

L.A. Stevens Valuation Model

L.A. Stevens Valuation Model

Summary of results:

Pre Q4 2021

Post Q4 2021

Fair Value Estimate

$53

$53 [No change]

2031 Price Target

$236

$236 [No change]

Shift remains a high-risk, high-return bet. While the cash burn situation is complicated (bankruptcy is possible in the next 12-18 months if no capital is raised), Softbank’s investment in Shift during Q4 is a very positive development. Shift’s management is confident about the company’s path to profitability and its ability to attract institutional investors (like Softbank) for future capital raises. My analysis and available evidence tell me that Shift’s management is more than likely to be right.

Considering the asymmetric risk/reward opportunity and management’s execution history, I am more bullish than ever on Shift. I am happily buying more here at these depressed levels. Shift is truly a VC bet, and it could take years to pay off, so tighten your seat belts for this bumpy ride to glory. Please limit your position size to our maximum suggested portfolio weight of 1.25% (of AUM) as the bankruptcy risk is genuine.

Key takeaway: I rate Shift a strong buy at ~$2.5 per share.

If you have any thoughts/questions/concerns, please share them in the comments section below or in the chats.

At Beating The Market, we focus on making lives meaningfully better through investing. To join a rapidly growing community of like-minded, long-term growth investors –> Click Here

This article was written by

Ahan Vashi is the Head of Equity Research at L.A. Stevens Investment LLC’s Seeking Alpha Marketplace service – Beating The Market. He is a “Quantamental” investor who specializes in identifying market-beating stocks by capitalizing momentum of business fundamentals. Some of his top picks include Upstart at $58, Palantir at $9, and Asana at $22.

Prior to joining L.A. Stevens Investments, Ahan worked as an Associate Fellow with Jacmel Growth Partners, a middle-market private equity firm where he acquired the art of analyzing financial statements and business valuation. Ahan holds a Master of Quantitative Finance degree from Rutgers Business School and a Bachelor of Technology degree in Electronics and Communication Engineering from NIT, Surat.

At Beating The Market, Ahan works with Louis Stevens, Jared Simons, and one of the most vibrant and dynamic investment communities on earth in pursuit of identifying the next Facebook, Amazon, and Salesforce. Beating The Market brings the potent wealth-creating power of Venture Capital to the public markets. For his part on the team, Ahan does this by systematically analyzing hundreds of public companies each year via BTM’s rigorously defined set of 23 standards/criteria – BTM’s Crucial Characteristics.

In addition to high-growth companies, Ahan works on identifying dividend-growth stocks that can deliver supercharged returns with low volatility via massive capital return programs (dividends and buybacks). Most of Ahan’s public articles tend to focus on this area, while his research on high-growth companies is available exclusively to members of Beating The Market.

If you’d like “Ahan-lite”, check out his Twitter profile here: https://twitter.com/VashiAhan

If you have any questions, feel free to reach out to him via a direct message on SA or leave a comment in one of his articles!

Disclosure: Ahan Vashi is a promoting contributor for Louis Stevens’ SA Marketplace service – Beating The Market

Disclosure: I/we have a beneficial long position in the shares of SFT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.