Alistair Berg

Alistair Berg

That which can be asserted without evidence, can be dismissed without evidence.“― Christopher Hitchens

Today we take a deeper look on a small cap concern in the online learning space. After coming public in 2021, the shares find themselves deep in “Busted IPO” territory, like most of that IPO “vintage.” The decline has triggered some big insider purchases from the company’s founder. A full analysis follows below.

Seeking Alpha

Seeking Alpha

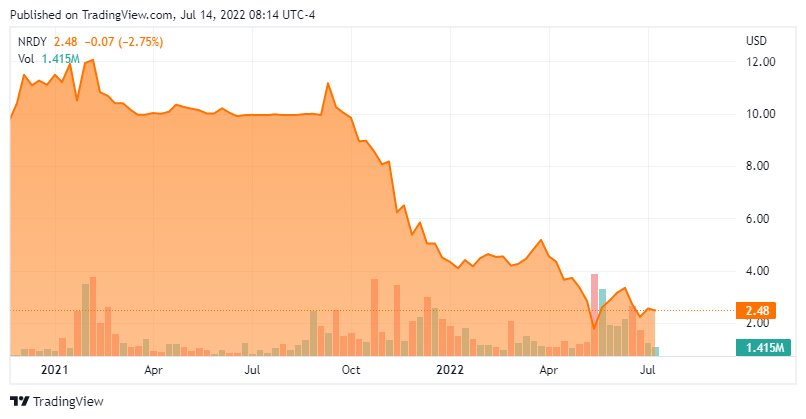

Nerdy, Inc. (NYSE:NRDY) is a St. Louis, Missouri-headquartered online learning platform with offerings encompassing K-8, high school, college, graduate school, and professional licensing. In FY21, the company hosted 1.92 million paid online sessions covering over 3,000 subjects. Nerdy was formed in 2007 as Live Learning Technologies and went public through a reverse merger into special purpose acquisition company (SPAC) TPG Pace in September 2021, with its first transaction as a public concern conducted at $10.96 a share. The stock trades just north of three bucks a share, translating to a market cap of approximately $400 million.

The company is capitalized by two classes of stock. The 90.5 million shares of publicly traded Class A stock confer economic interest and one vote per share, while the 68.5 million shares of privately held Class B stock bestow no economic interest but enjoy similar voting rights and are convertible into Class A shares. Owing to this arrangement, Founder, Chairman, & CEO Charles Cohn beneficially owns 29% of the voting rights and through his holdings can elect three members to the board.

Nerdy’s flagship offering is Varsity Tutors, which matches what the company dubs “Learners” with “Experts” for one-on-one, small-class, or large-class instruction. One-on-one tutoring is purchased by the hour and can be used in blocks of 15 minutes. This format is by far and away the company’s largest revenue generator, responsible for 83% of total in 2021. In 1Q22, Nerdy launched a monthly membership program as a complement to its current front-weighted pay-by-the-hour sales model, whereby customers pay a fixed monthly rate for a term of 3 to 36 months for one to three sessions per week. Monthly prices for a once-a-week contract are ~$200 to $325 per month. This structure makes it easier for potential students to afford sessions by avoiding a large upfront outlay.

Small class formats offer live teacher-student interaction with a maximum class size of 20. Large online group classes are typically 500 to 50,000+ in size, cover a variety of topics, are sometimes taught by celebrity Experts, and are provided free of charge. The large classes are designed to generate brand awareness and familiarize Learners with Nerdy in hopes of converting them into paying customers.

Furthermore, the company offers learning-as-a-platform solutions to institutions that can be customized by service and product offerings. It includes tutoring from one to five Learners at a time and uses diagnostic assessments to group individuals with similar proficiencies with an instructor. Nerdy also employs an AI matching algorithm that analyzes attributes of both Learners and Experts to identify Learner-Expert matches with the highest projected probability of a successful interaction.

Employing this approach, Nerdy’s realized FY21 revenue of ~$1,100 per Active Learner, defined as any individual who attended a paid online one-on-one instruction, paid small online class, or paid group tutoring session. Most vetted instructors are independent contractors who get their side hustle on from their home or classroom and count as cost of goods sold for the company. Students seem very satisfied with the offerings provided by Nerdy, giving it a net promotor score of 68 in FY20.

The market for the company’s offering is substantial, with global supplemental education (excluding that which is government-funded) estimated at $1.3 trillion in 2020. Approximately 98% of this interaction remains offline. It goes without saying that the pandemic created a significant opportunity to expose students and their parents to online education. Although the post-pandemic return of students to the classroom is welcomed by nearly all, the online experience created significant tailwinds for the idea of paid online tutoring versus the more inefficient in-person model.

Nerdy estimates that its domestic U.S. direct-to-consumer learning total addressable market (“TAM”) was ~$47 billion in 2019 and will expand to ~$62 billion by 2024. In addition to in-person learning models pioneered by the likes of Sylvan Learning and Kaplan, the company competes with asynchronous (non-live) online offerings from Coursera (COUR) and Udemy (UDMY). However, Nerdy differentiates itself with its offerings that are both live and online.

With its scalable, direct-to-consumer online education platform encompassing 87,000 learners and 20,000 experts offering instruction on ~3,000 subjects with a significant TAM that is shifting to virtual, Nerdy’s stock seemed poised for success when it began trading on the NYSE. However, after reaching $13.49 a share the day after its public debut, Nerdy’s stock has crashed 79% due to a confluence of circumstances, two of which were the dominance of the risk-off trade and the market’s continuing contempt for anything birthed by a SPAC. To be sure, the selloff in NRDY shares was also self-inflicted.

1Q22 Earnings & Outlook

It started with its first earnings report (3Q21) as a public concern in November 2021, when it posted revenue of $31.3 million versus consensus/guidance of $35.7 million. That disappointment was followed by its 4Q21 earnings release in late February 2022, in which Nerdy guided FY22 revenue to a consensus 41% increase to $198 million; however, its Adj. EBITDA guide was below consensus at negative $22.5 million. By the time the company announced its 1Q22 financial results on May 16, 2022, it could be argued that additional bad news was already baked in, with shares of NRDY trading at $2.57.

May Company Presentation

May Company Presentation

That assessment proved inaccurate after Nerdy reported a non-GAAP net loss of $8.2 million and Adj. EBITDA of negative $6.6 million on revenue of $46.9 million versus a non-GAAP net loss of $3.2 million and Adj. EBITDA of negative $0.3 million on revenue of $34.6 million in 1Q21. The 36% year-over-year improvement at its top line was in-line and revenue bookings of $48.5 million (up 30%) in the quarter were slightly better than consensus. Active Learners were up 56% and Active Experts were up 37% versus 1Q21, which translated to a 57% increase in learning sessions. Furthermore, gross margin improved 220 basis points to 69.8%.

The problem for Nerdy was its revised outlook for FY22, the headline of which was a new top-line forecast of $167.5 million, down 15% from its first estimate of $198 million. Adj. EBITDA was also revised down $10.5 million to $33 million. (Both metrics based on range midpoints.) Management stated that it was to reflect its shift toward a membership format, where revenue recognition is not frontloaded but spread out equally over the life of the subscription. It also slipped in that it experienced a decrease in bookings growth rates in March and April (after a positive trend in January and February) and was now expecting heightened summer travel to act as a revenue headwind.

Not surprisingly, the market took Nerdy behind the woodshed, selling its stock down 25% in the subsequent trading session and eventually 38% (to $1.59 a share) on May 19th.

On the bright side, the company’s balance sheet is pristine, with cash and equivalents of $141.7 million and no debt as of March 31, 2022. Despite its $8.2 million non-GAAP loss, it only burned through cash from operations of $0.9 million.

Street analysts have been mostly constructive (and wrong) on Nerdy’s stock, featuring two buys and five outperforms against two holds. One of those two holds came via a Goldman Sachs’ downgrade from a buy after its most recent earnings report. The median analyst price target is around $5.50 a share. They expect Nerdy to lose $0.59 a share (non-GAAP) on revenue of $167 million in FY22, followed by a loss of $0.43 a share (non-GAAP) on revenue of $213 million.

After the earnings report, CEO Cohn went on a substantial buying spree, purchasing 3.83 million shares of NRDY for three of his family’s trusts at an average price of $2.20 and now owns just over a third of the outstanding float. His CFO (27,000 shares at $1.86) and Chief Legal Officer (12,500 at $1.70) also bought, albeit more modestly.

Supported by Cohn’s accumulation, Nerdy’s stock has rallied some 60% off its all-time low of $1.59 a share in two weeks. It now trades at 1.5x FY22E revenue net of cash which, owing in large measure to its introduction of a membership model, will only grow 25% over FY21. However, once that model fully cycles through its income statement, its top-line growth should accelerate from there.

That said, in this risk-off environment with no prospects for profitability for at least 30 months, a likely retest of $2 could occur once it has been determined that Cohn has completed his purchases – or at least entered a blackout period. Therefore, I would not chase this name at this time. Considering the substantial option premium, Nerdy does becomes attractive as a covered call candidate at or below $2.50 a share.

Humor is reason gone mad.”― Groucho Marx

Author’s note: I present and update my best small-cap Busted IPO stock ideas only to subscribers of my exclusive marketplace, The Busted IPO Forum. Try a free 2-week trial today by clicking on our logo below!

This article was written by

The Busted IPO Forum founded by Bret Jensen, is a hypothetical $200K portfolio built of stocks that have been public for 18 months to five years that are significantly under their offering price. Many times after the initial analyst hyperbole has died and lockups have expired, these same companies can be had for .30 to .50 cents on the dollar from when the shares went public. As lucrative as this niche has been for my portfolio over the years, a service or newsletter has not existed that covered this segment of the market — until now! The goal in creating the Busted IPO Forum is to build a portfolio of 15-20 small cap and mid cap busted IPOs which consistently outperform the Russell 2000 over time. As of 07/02/2021 our model portfolio has generated an overall return of 73.84% substantially above the 52.37% gain from the Russell 2000 over the same time frame.

• • •

Specializing in profiling high beta sectors, Bret Jensen founded and also manages The Biotech Forum, The Insiders Forum, and the Busted IPO Forum model portfolios. Finding “gems” in the biotech and small-cap stock sectors, these highly volatile spaces proven hugely successful have empowered Bret Jensen’s own investing portfolio.

• • •

Learn more about Bret Jensen’s Marketplace offerings:

The Insiders Forum | The Biotech Forum | Busted IPO Forum

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in NRDY over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Bret Jensen is the Founder of and authors articles for the Biotech Forum, Busted IPO Forum and Insiders Forum.