Drew Angerer/Getty Images News

Drew Angerer/Getty Images News

The week of July 25 will be a big one for markets, with the FOMC meeting on Wednesday afternoon. I noted last weekend that the markets could be due for a significant drop, and I still think that is likely to happen. Unfortunately for me, it seems as if my timing may have been off by a few days because the VIX fell all week.

That leaves one to believe that either the market is playing a game or extremely complacent, heading into a pivotal week. The VIX index (VIX) is trading around 23 at its lowest level leading into an FOMC meeting this year. The day before the previous four FOMC meetings in 2022, the VIX closed above 29 every time. So not only is the VIX low ahead of the FOMC meeting, but if it stays at this level or goes lower, it will be exceptionally low. So either this is a trap that the market is setting up for the bulls, or this market is completely underestimating the importance of this week’s FOMC meeting.

Trading View

Trading View

Additionally, the VIX is now very oversold and even trading below its lower Bollinger band, suggesting the index may be close to a low point and due for a big spike to the upper side of its Bollinger band.

Trading View

Trading View

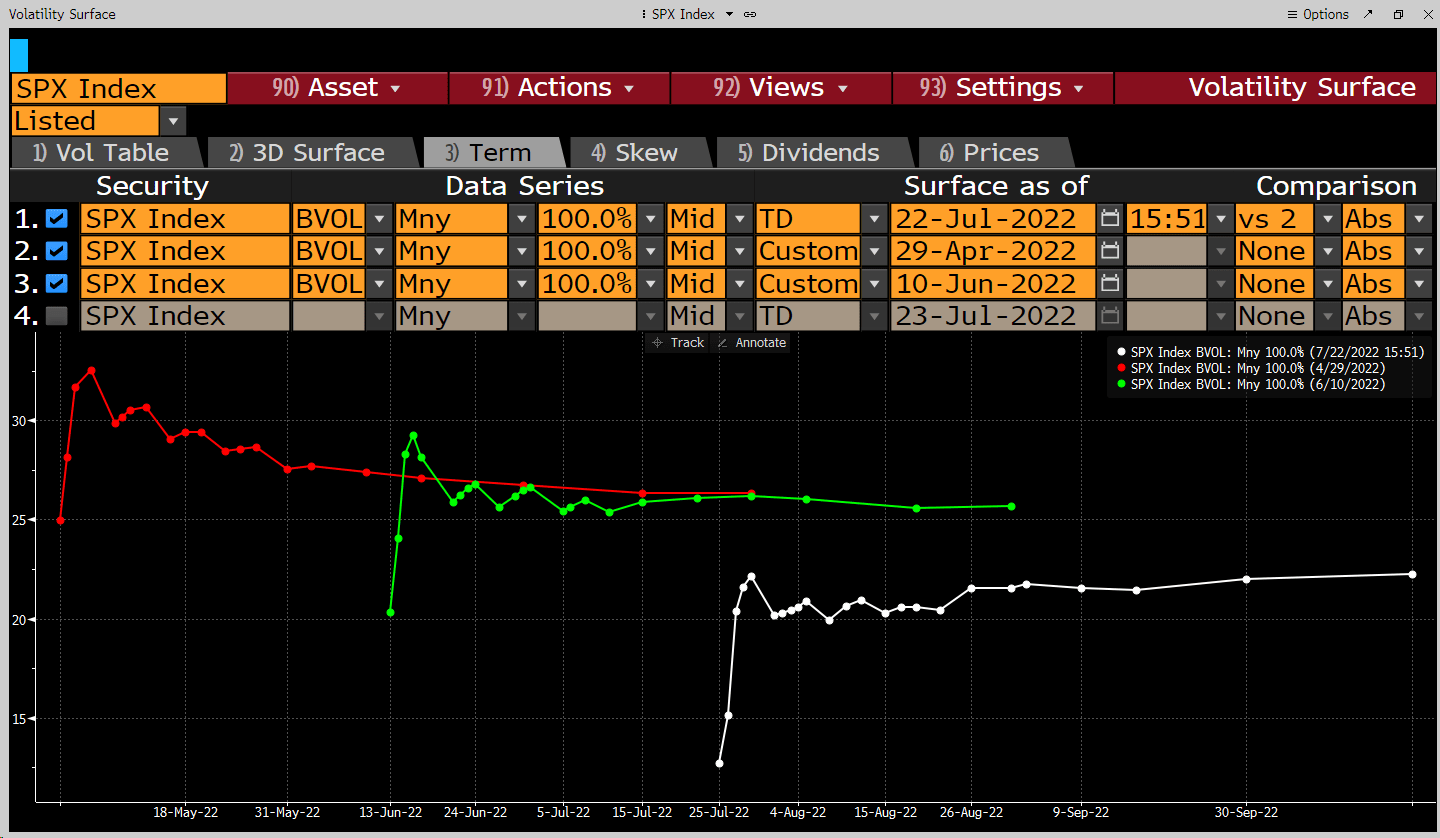

One can turn to the implied volatility term structure of the S&P 500 options to better understand how complacent the market is. When looking at this term structure and comparing the current structure with the Friday before the June FOMC meeting, one can see that the existing term structure is significantly lower.

An at-the-money option for the June 15 expiration date had an implied volatility of around 28.5% on June 10. As of July 22, an at-the-money option for the July 27 expiration has an implied volatility level nearly 8% percentage points lower, at 20.4%. The market appears not to be taking this week’s event as seriously as in the past. Heading into the May FOMC meeting, an at-the-money option for the May 4 expiration date was at 31.9%, making the implied volatility difference between the May and June FOMC meeting just 3.4%.

Given the low implied volatility levels, the market appears to be taking this meeting almost as a non-event.

Bloomberg

Bloomberg

This complacency may be happening because the market has convinced itself that the Fed is close to pivoting, caving in, and going back to its old ways of supporting asset prices. This week’s meeting may change the market’s mind on how serious the Fed is regarding its battle against inflation and that it doesn’t view the economy as weak or heading for a recession.

Chris Waller, a member of the FOMC board, recently gave an interview and was explicitly asked about the potential for a second quarter of negative GDP growth. In that interview, Waller revealed that the gross domestic product and gross domestic income were diverging and that while GDP was trending lower, GDI was not. He noted that these two measures of the economy are supposed to trend in the same direction and believes that GDP at some point is likely to be revised higher, and perhaps GDI is likely to be adjusted a little bit lower. But the strength of the labor market and the GDI numbers would suggest the economy is not in a recession nor heading towards one. He also noted that the negative GDP prints might be due to measures of the export category that are undermining how the domestic side of the economy is doing.

Looking at this closer, while real GDP was negative in the first quarter, real GDI was up 1.8%. This suggests that perhaps the economy wasn’t as weak as the GDP report presented. If the Fed considers these other factors, such as the GDI when considering the economy’s growth and strength, that could be problematic for a market now expecting a Fed pivot.

FRED

FRED

Ironically or not, this topic came of GDP and GDI came up in the latest FOMC minutes, with participants noting the conflicting signals between the GDP and GDI regarding the pace of economic growth and that the labor market was very tight.

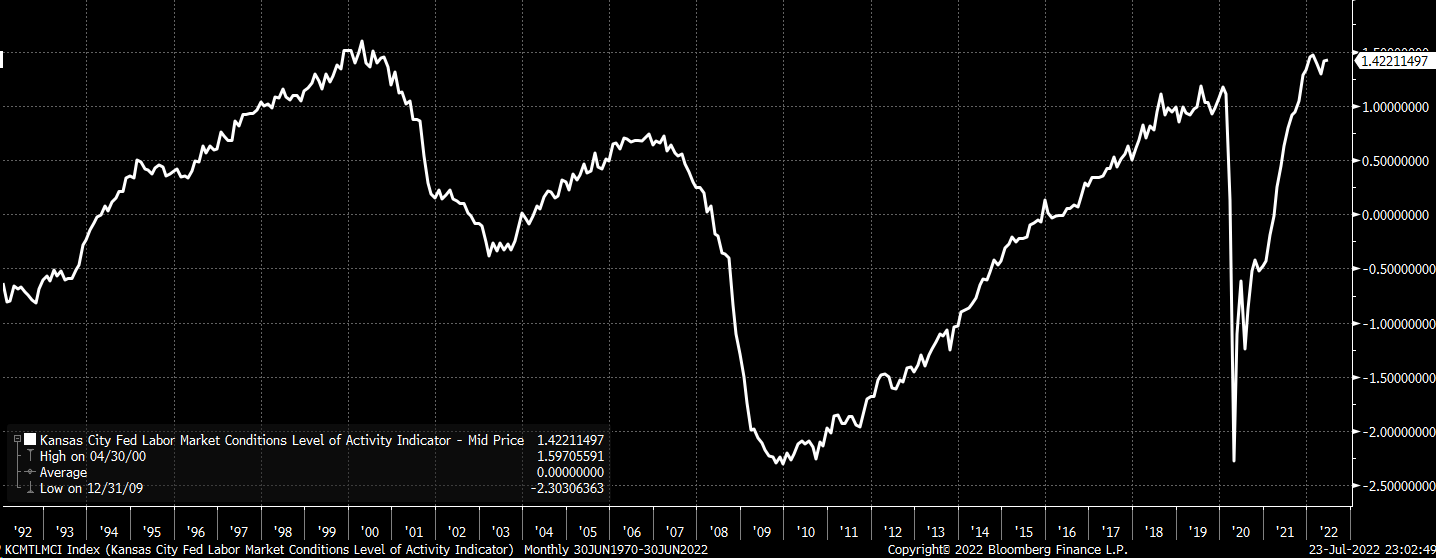

When digging into this further, the latest data from the Kansas City Labor Market Conditions Index, as of June 30, showed the index was still at its highest level since the late 1990s.

Bloomberg

Bloomberg

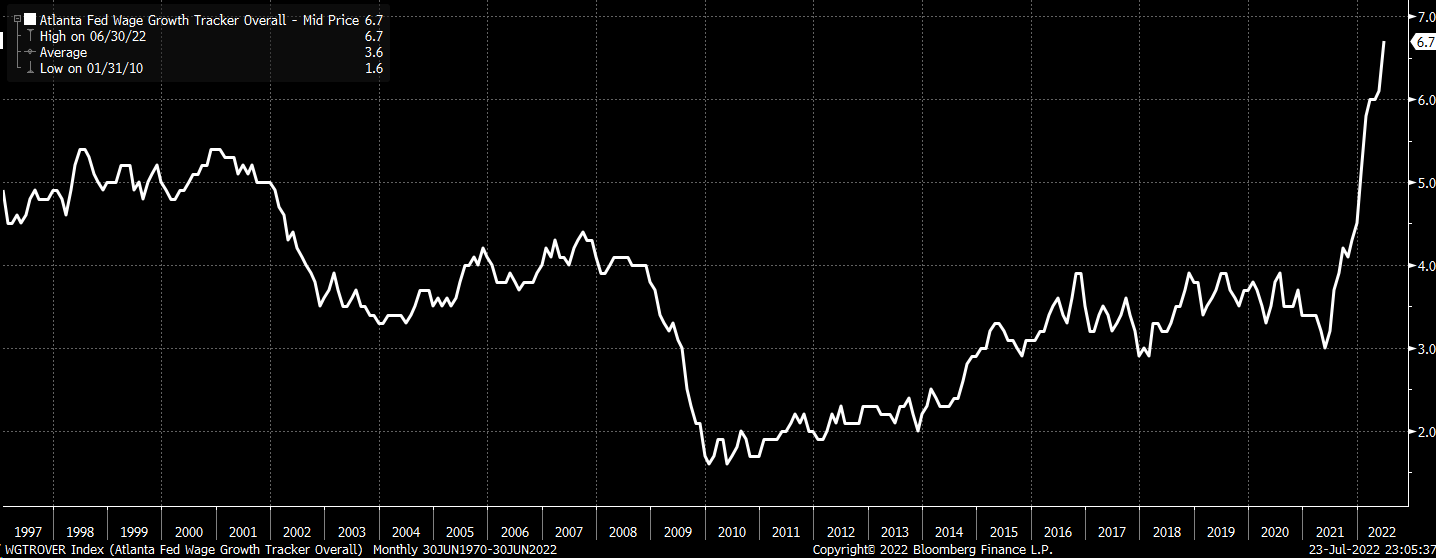

Additionally, the Atlanta Fed Wage growth tracker reached a new high at the end of June. That was its highest level recorded since 1997. At this point, the tracker has been rising vertically and is not showing signs of a peak yet.

Bloomberg

Bloomberg

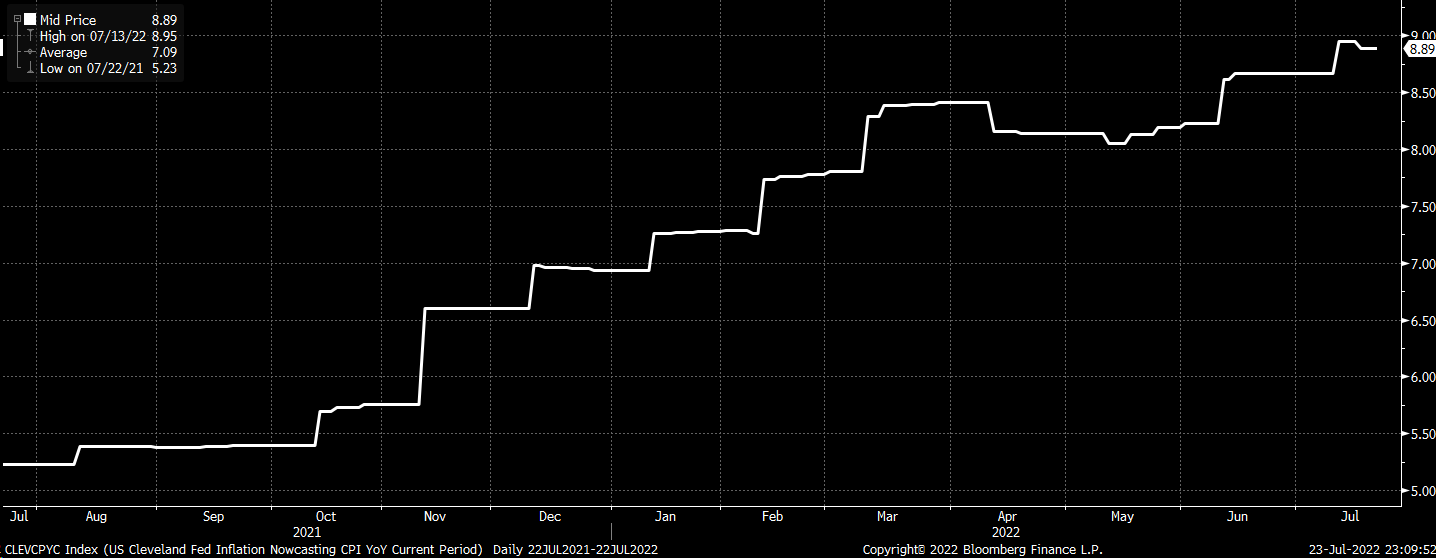

Even the Cleveland Fed CPI nowcast is forecasting a y/y CPI rate of change at 8.9% in July, which would be just two-tenths of a percent less than the June CPI’s 9.1% rate of change.

Bloomberg

Bloomberg

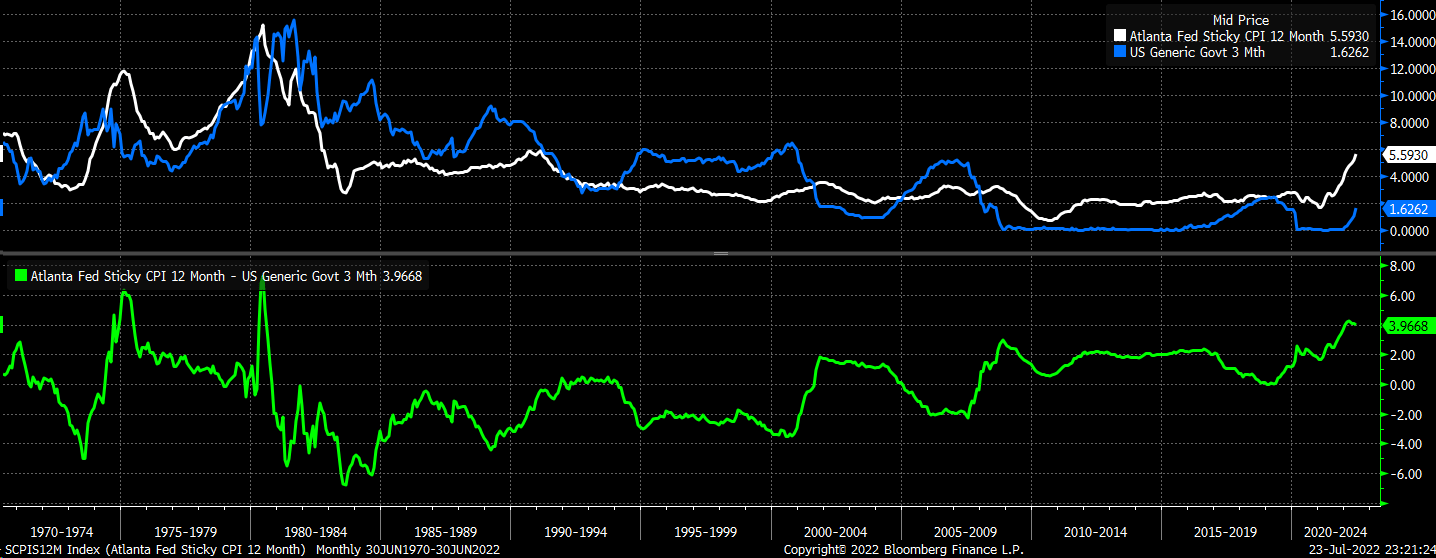

Meanwhile, the Atlanta Fed Sticky 12-month inflation forecast is currently at 5.6% and, like many of the indicators mentioned, is rising sharply and vertically. The last time this index saw a reading this high for sticky inflation was April 1991, when the three-month Treasury rate was almost 5.7%. The spread between the sticky measure of inflation and the 3-month Treasury bill was last this wide in July 1980.

Bloomberg

Bloomberg

What this all gets at is that, to this point, the Fed has had nearly no impact on its mandate of bringing inflation back to its 2% target, and the Fed can find plenty of metrics to use to brush aside worries of slowing growth if they so choose to reach their inflation goal.

The other point is that if inflation is becoming as sticky and entrenched as some of this forecast suggests. Rates may need to go even higher than what the Fed has currently protected, and a couple of quarters of negative inflation-adjusted real GDP will not slow them down.

If this is the message delivered this week by the Fed, then the stock market is not only too complacent, it will be in for a big shock.

Investing today is more complex than ever. With stocks rising and falling on very little news while doing the opposite of what seems logical. Reading the Markets helps readers cut through all the noise delivering stock ideas and market updates, looking for opportunities.

We use a repeated and detailed process of watching the fundamental trends, technical charts, and options trading data. The process helps isolate and determine where a stock, sector, or market may be heading over various time frames.

To Find Out More Visit Our Home Page

This article was written by

I am Michael Kramer, the founder of Mott Capital Management and creator of Reading The Markets, an SA Marketplace service. I focus on macro themes and trends, look for long-term thematic growth investments, and use options data to find unusual activity.

I use my over 25 years of experience as a buy-side trader, analyst, and portfolio manager, to explain the twists and turns of the stock market and where it may be heading next. Additionally, I use data from top vendors to formulate my analysis, including sell-side analyst estimates and research, newsfeeds, in-depth options data, and gamma levels.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Charts used with the permission of Bloomberg Finance L.P. This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice.Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.