MoMo Productions/DigitalVision via Getty Images

MoMo Productions/DigitalVision via Getty Images

Coursera, Inc. (NYSE:COUR) went public in March 2021, raising around $519 million in gross proceeds in an IPO that was priced at $33.00 per share.

The firm operates an online learning platform for a variety of end-user markets worldwide.

While COUR’s beaten-down stock price may present a value opportunity for patient, long-term investors who believe in its international approach and greater focus on Enterprise clients, for the near term I’m on Hold for COUR until it makes progress toward operating breakeven.

Mountain View, California-based Coursera was founded to develop an e-learning platform for consumers, academic institutions, businesses and governments.

Management is headed by Co-founder and Chairman, Andrew Ng; and President and CEO, Jeffrey Maggioncalda, who has been with the firm since 2017 and was previously CEO of Financial Engines (FNGN).

The company’s primary offerings & capabilities include:

Large content catalog

Machine learning

Personalized education

The company pursues consumer learners through its online presence and seeks industry, academic and government clients through direct sales and marketing efforts.

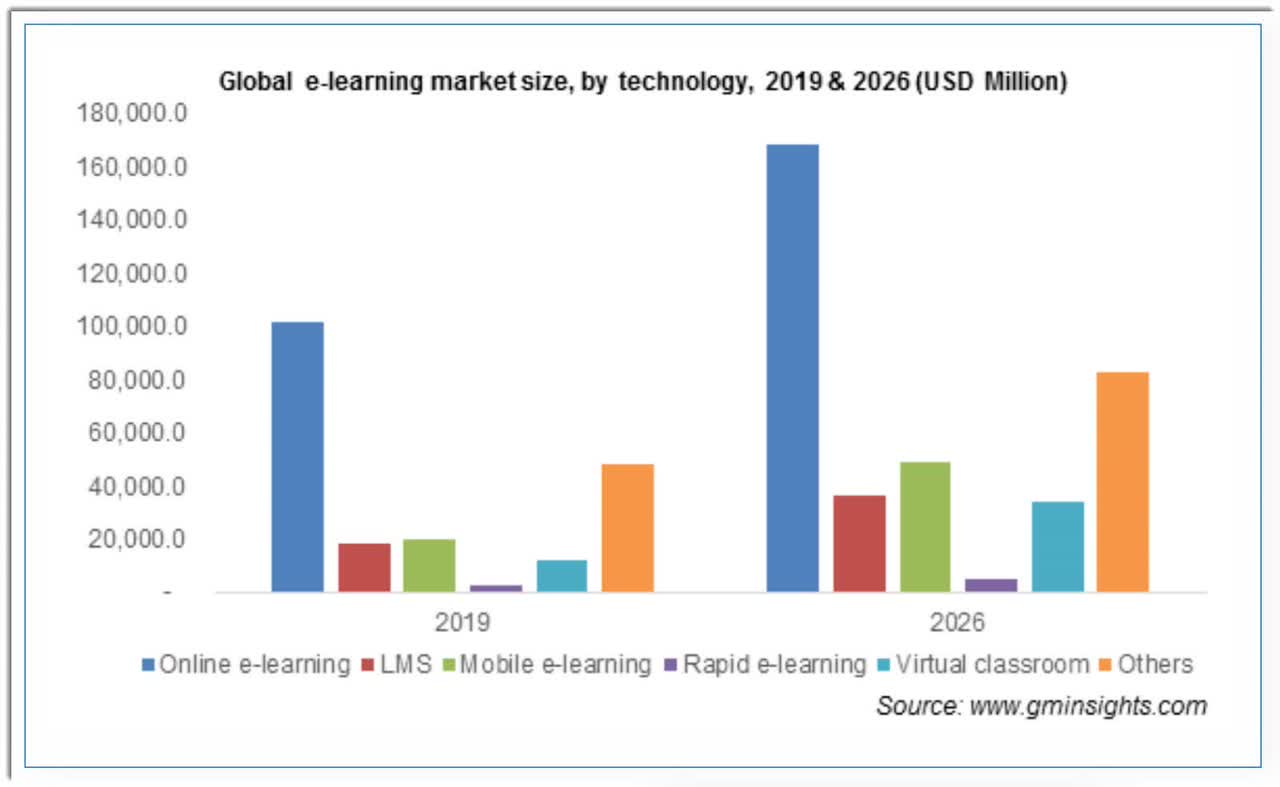

According to a 2020 market research report by Global Market Insights, the global market for e-learning services is expected to reach $375 billion in value by the end of 2026.

This represents a forecast CAGR of 8.0% from 2020 to 2026.

The main drivers for this expected growth are continued technological innovation and growing Internet usage worldwide.

Also, the COVID-19 pandemic has acted as a forcing function for many users to pursue their education in an online environment, likely increasing the industry’s growth prospects in the years ahead.

Below is a chart showing the expected growth in the market by technology:

Global E-Learning Market (Global Market Insights)

Global E-Learning Market (Global Market Insights)

Major competitive or other industry participants include:

2U (TWOU)

edX

Eruditus Learning Solutions

FutureLearn

Udemy (UDMY)

upGrad Education

Degreed

A Cloud Guru

LinkedIn (MSFT)

Pluralsight (PS)

Udacity (UCITY)

Khan Academy

Google (GOOG)

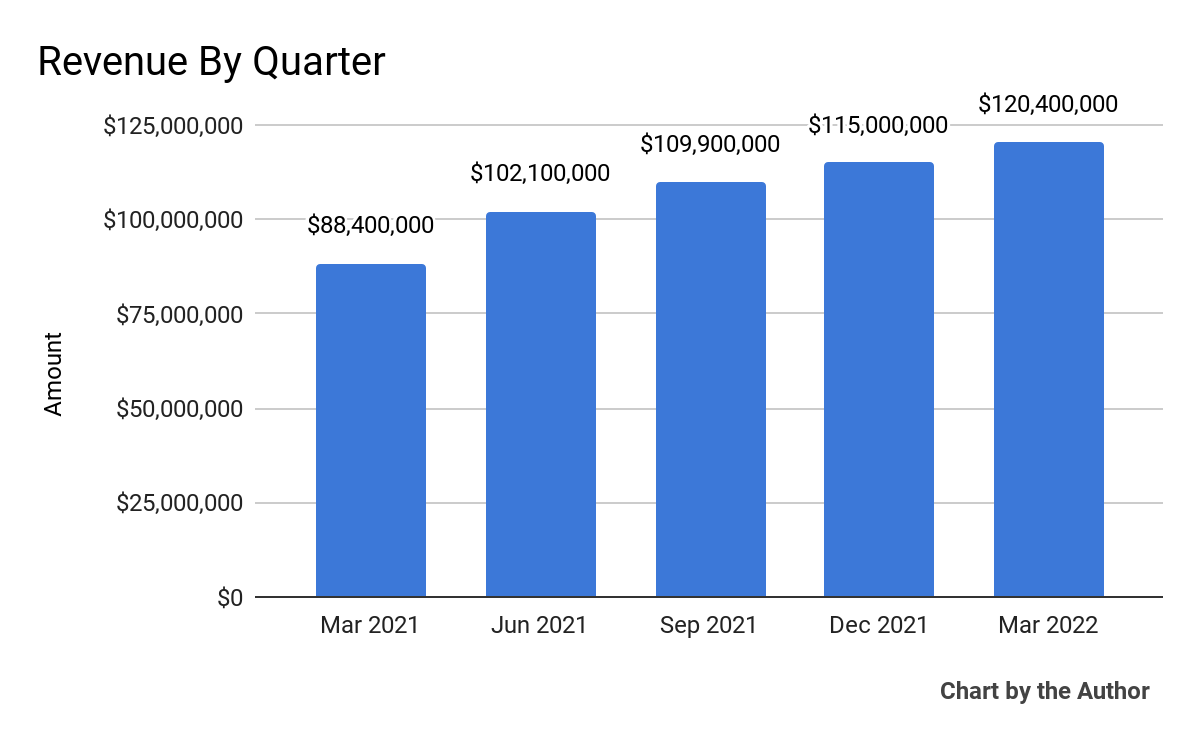

Topline revenue by quarter has grown steadily over the past 15 quarters:

5 Quarter Total Revenue (Seeking Alpha and The Author)

5 Quarter Total Revenue (Seeking Alpha and The Author)

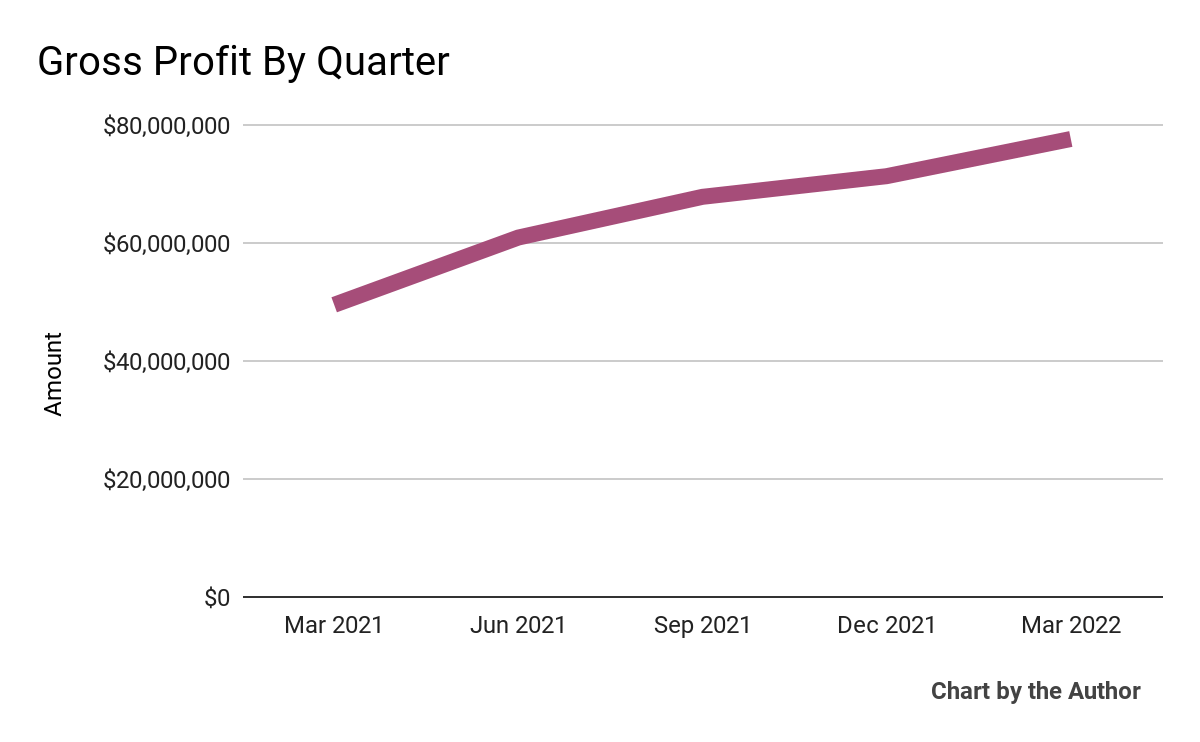

Gross profit by quarter has followed approximately the same trajectory as total revenue:

5 Quarter Gross Profit (Seeking Alpha and The Author)

5 Quarter Gross Profit (Seeking Alpha and The Author)

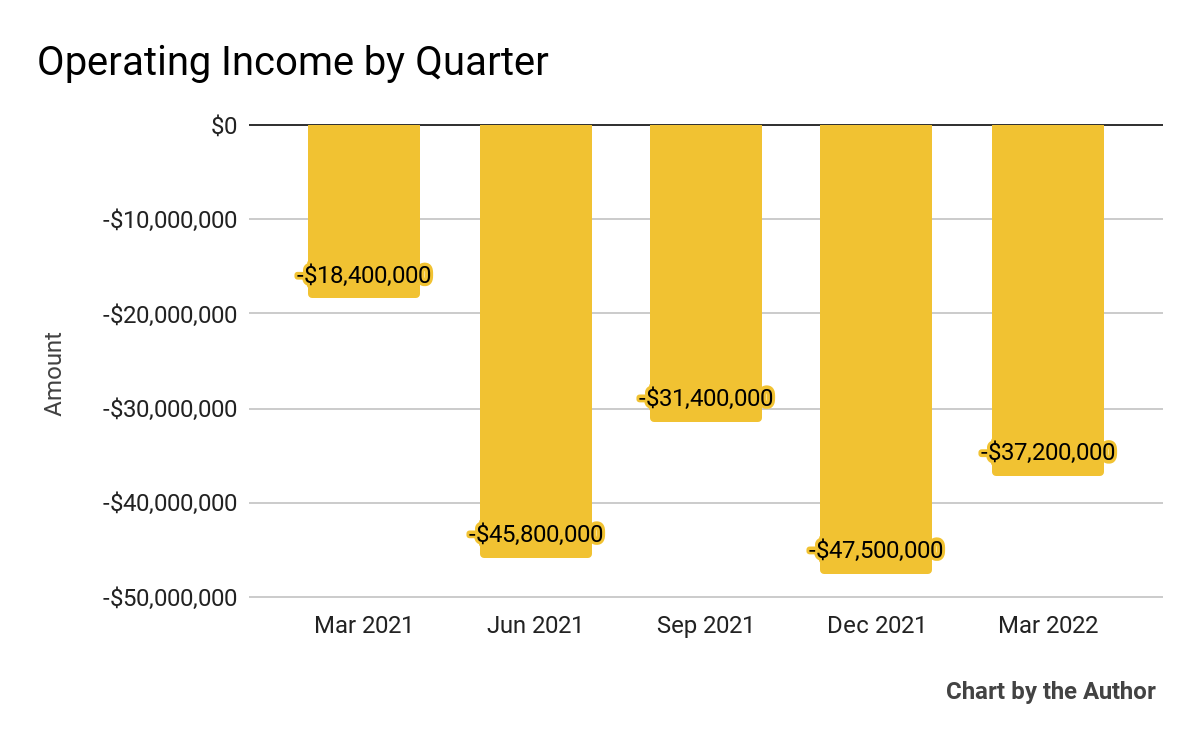

Operating income by quarter has remained heavily negative:

5 Quarter Operating Income (Seeking Alpha and The Author)

5 Quarter Operating Income (Seeking Alpha and The Author)

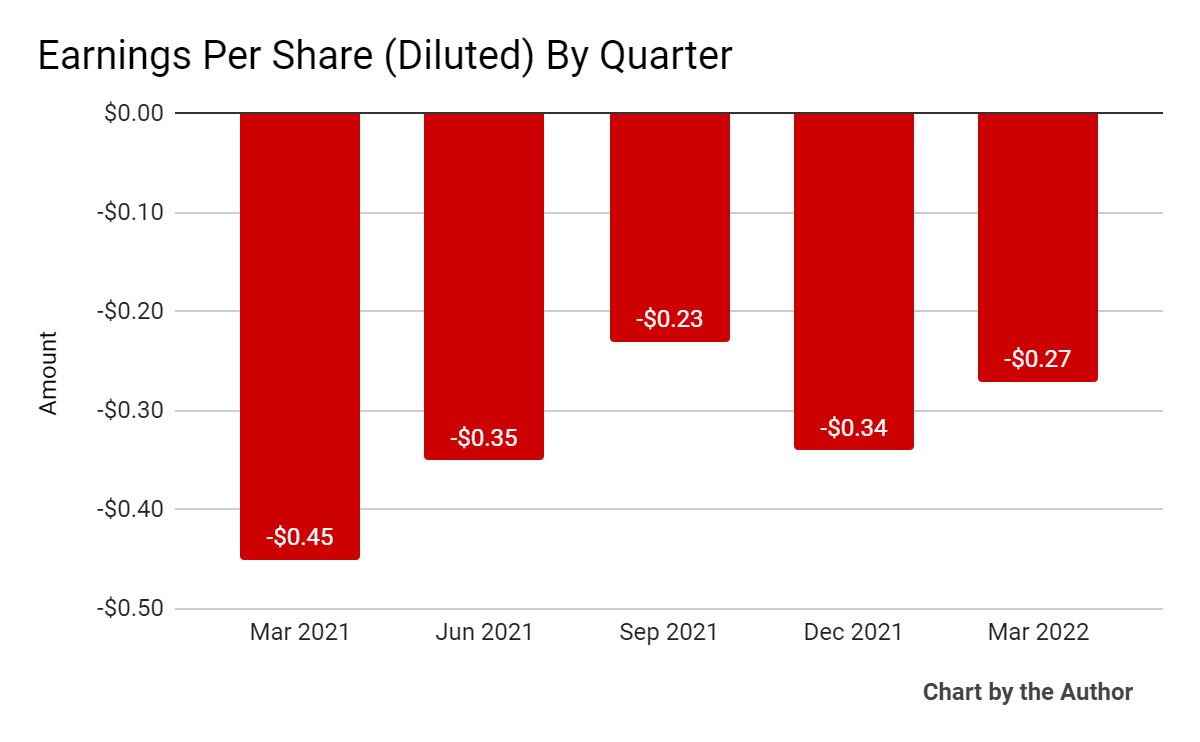

Earnings per share (Diluted) have also remained substantially negative in recent quarters, with no obvious path to breakeven:

5 Quarter Earnings Per Share (Seeking Alpha and The Author)

5 Quarter Earnings Per Share (Seeking Alpha and The Author)

(Source data for above GAAP financial charts)

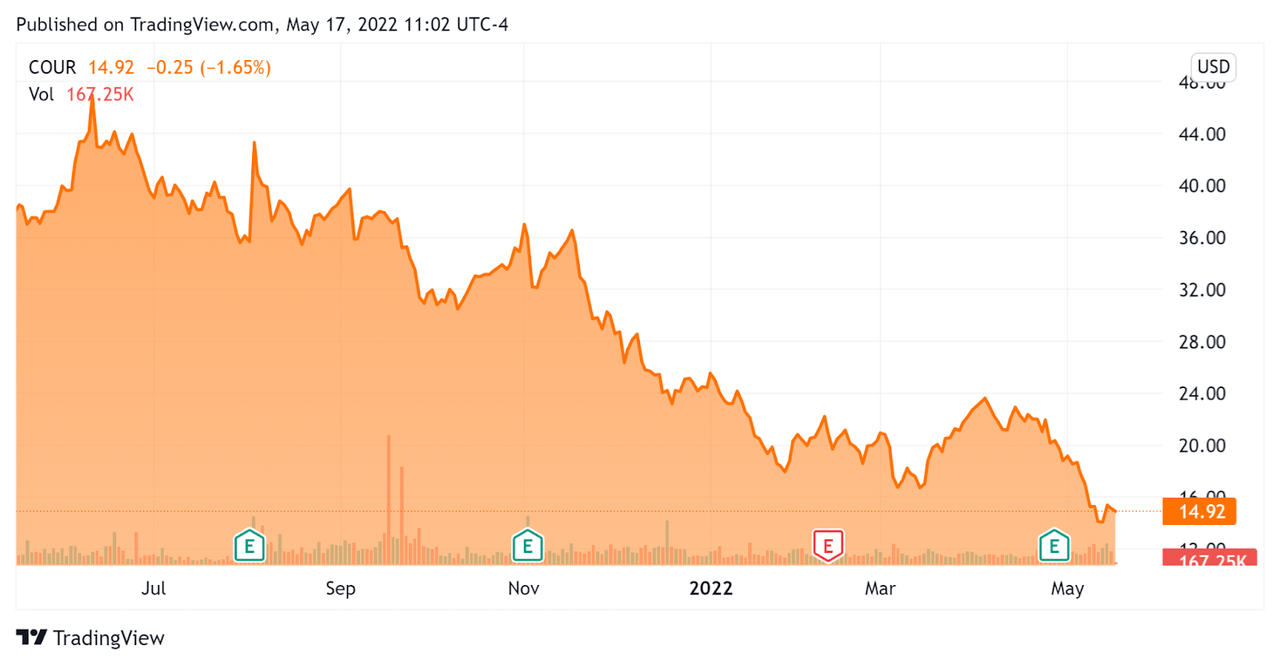

In the past 12 months, COUR’s stock price has dropped 60.6 percent vs. the U.S. S&P 500 index’s fall of 2.8 percent, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

52 Week Stock Price (Seeking Alpha)

Below is a table of relevant capitalization and valuation figures for the company:

Measure

Amount

Market Capitalization

$2,220,000,000

Enterprise Value

$1,450,000,000

Price/Sales

4.71

Enterprise Value/Sales

3.25

Enterprise Value/EBITDA

-9.97

Operating Cash Flow (TTM)

-$32,160,000

Revenue Growth Rate (TTM)

36.38%

Earnings Per Share

-$1.19

(Source)

As a reference, a relevant public comparable would be Udemy; shown below is a comparison of their primary valuation metrics:

Metric

Udemy (UDMY)

Coursera (COUR)

Variance

Price/Sales

2.60

4.71

81.2%

Enterprise Value/Sales

2.23

3.25

45.7%

Enterprise Value/EBITDA

-17.39

-9.97

-42.7%

Operating Cash Flow (TTM)

-$7,320,000

-$32,160,000

339.3%

Revenue Growth Rate

19.7%

36.4%

84.3%

(Source)

In its last earnings call (transcript), covering Q1 2021’s results, management highlighted the milestone of exceeding 100 million registered users on the site.

CEO Maggioncalda spoke of the company’s 3-sided marketplace (students, teachers and institutions) and the addition of notable additions to its institutional partners.

The company is also working with the University of Michigan to create 10 extended reality (augmented or virtual reality) “immersive learning experiences” exclusively for Coursera, with the pilot program scheduled to begin in early 2023.

As to its financial results, the firm grew revenue by 36% year-over-year, the 12th quarter in a row of more than a 30% growth rate.

Gross profit increased to nearly 65%, which was 9% higher than the previous year’s same period due to revenue mix and content cost containment.

However, sales and marketing costs grew 35% year-over-year as management has ramped up its pursuit of enterprise customers.

The company ended Q1 2022 with $780 million in unrestricted cash and used $42.2 million free cash in Q1, so has plenty of runway ahead of it.

Looking ahead, the CFO guided to only 31% topline revenue growth for the full year ahead.

Regarding valuation, the market is valuing COUR at higher multiples than comparable Udemy, likely due in part to COUR’s higher topline revenue growth rate and lower negative EV/EBITDA rate.

COUR has produced impressive topline revenue growth, no doubt aided by the COVID-19 pandemic trend of “work from home.”

But, the firm has made no meaningful progress to operating breakeven, producing significant and ongoing losses as it pursues growth during a period where the stock market is penalizing unprofitable growth in a rising interest rate environment.

While COUR’s beaten-down stock price may present a value opportunity for patient, long-term investors who believe in its international approach and greater focus on Enterprise clients, for the near term I’m on Hold for COUR until it makes serious progress toward operating breakeven.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis.

Get started with a free trial!

This article was written by

I’m the founder of IPO Edge on Seeking Alpha, a research service for investors interested in IPOs on US markets. Subscribers receive access to my proprietary research, valuation, data, commentary, opinions, and chat on U.S. IPOs. Join now to get an insider’s ‘edge’ on new issues coming to market, both before and after the IPO. Start with a 14-day Free Trial.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This report is intended for educational purposes only and is not financial, legal or investment advice. The information referenced or contained herein may change, be in error, become outdated and irrelevant, or removed at any time without notice. You should perform your own research for your particular financial situation before making any decisions. Post-IPO investing carries significant volatility and risk of loss.