gorodenkoff

gorodenkoff

Mega-caps have been popular among investors, and rightfully so. They have offered compelling returns in the past and are highly liquid. Two of those are active in the emerging autonomous driving space: Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) via its Waymo subsidiary, and Tesla (NASDAQ:TSLA), via its Autopilot/FSD program. In this article, we’ll look at the opportunities and risks of both companies to see which one is a more promising investment at current prices.

Both companies split their shares not too long ago, in a bid to bring down their share prices to a more “normal” level. Potential index inclusion in the Dow Jones, which is price-weighted, likely also played a role in their decisions to split their shares.

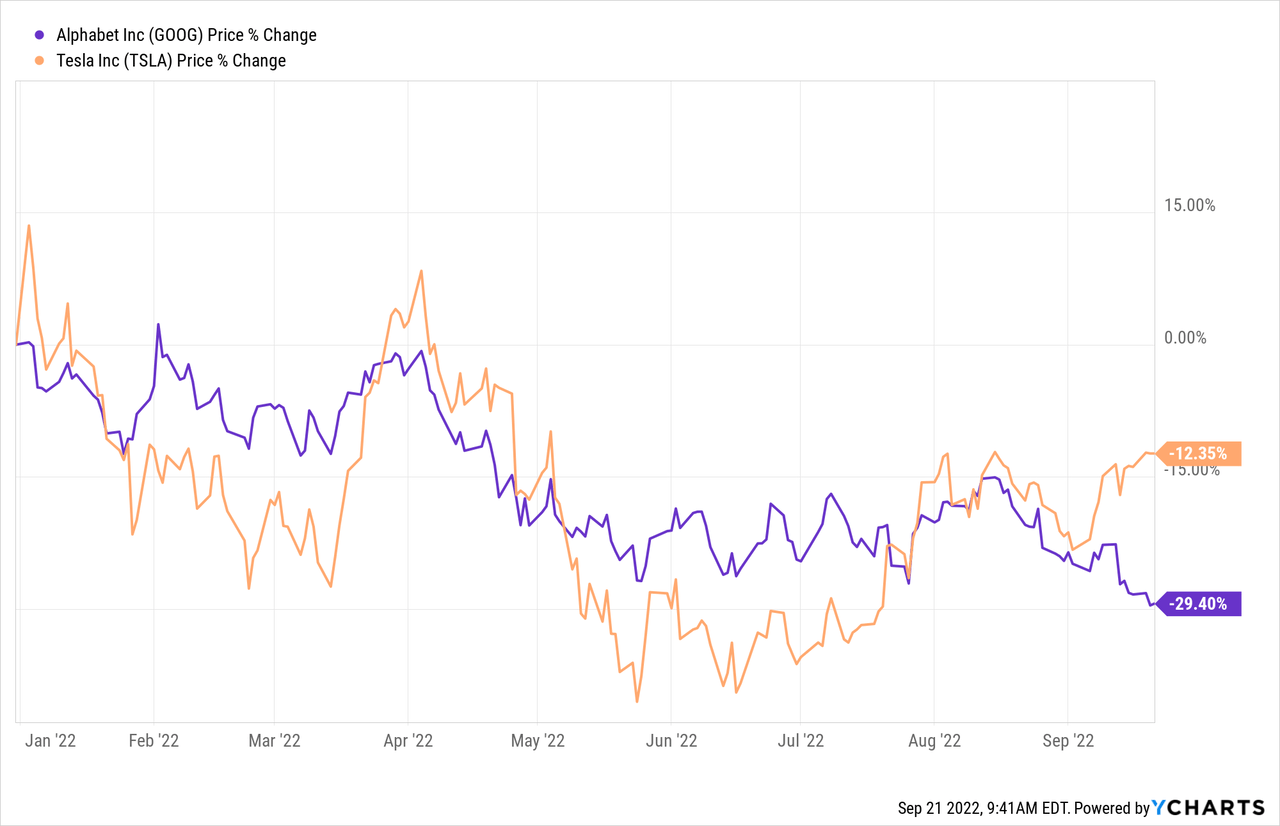

So far this year, both companies have seen their shares drop, with TSLA being down 12% while GOOG is down almost 30% in 2022. Alphabet split its shares in mid-July and has declined slightly since then, while Tesla split its shares in early August. Prior to that stock split, Tesla’s shares experienced a run-up, but since then, they moved mostly sideways. From a near-term share price perspective, these stock splits were thus not successful, but buying purely due to a stock split isn’t a great investment approach anyway.

The two companies aren’t competitors with everything they do, as Alphabet is mostly an online advertising company, while Tesla primarily is a car manufacturer. Nevertheless, the two compete in a prominent, fast-growing, and potentially very promising (in an economic sense) area, which is self-driving automobile technology.

Alphabet has been active in this space for quite some time via its Waymo subsidiary. Tesla has ambitious goals in this space as well, which it pursues via its self-driving tech program Autopilot/FSD.

No one knows when the first automobile with Level 5 self-driving technology will be available, or which company will produce it. But it is pretty clear that there are some companies that are in strong positions today and that could be important contenders for that title.

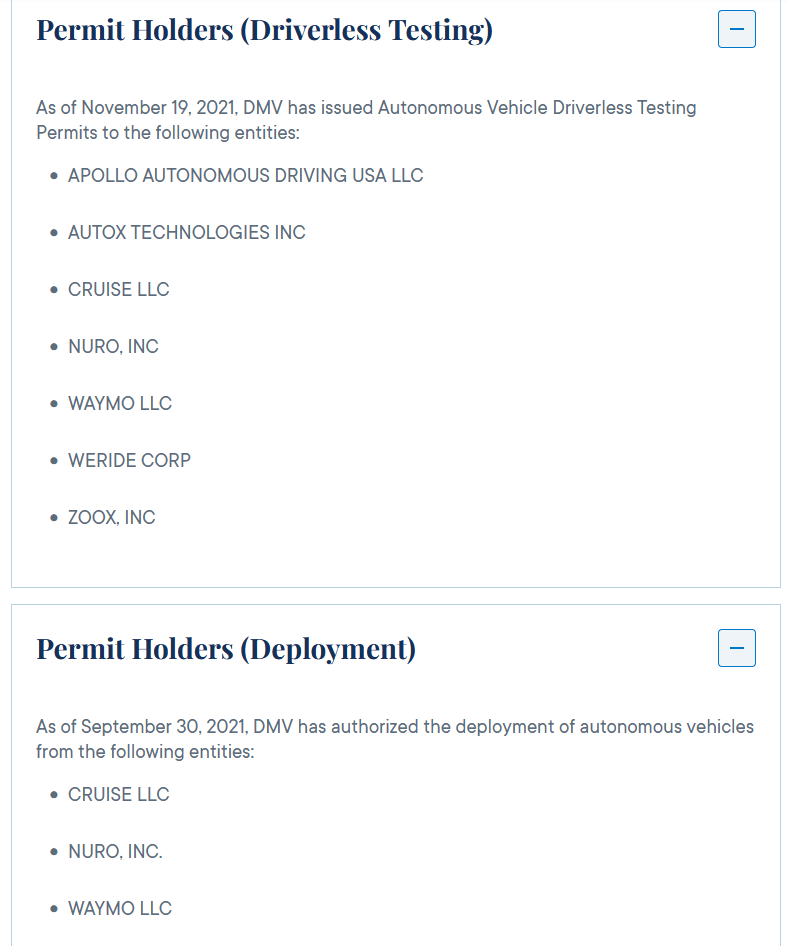

The following image shows a list of companies that have been approved for testing their vehicles in California without a driver. Some of those companies are even allowed to deploy their tech in the state:

ca.gov

ca.gov

We see that Google’s Waymo holds the permit in both groups, as do Nuro and GM’s (GM) Cruise. It seems reasonable to me to assume that the companies with the most advantaged permits are the companies with the most advantaged tech. A couple of other companies are allowed to test their tech in vehicles without a driver, including WeRide and Zoox. Notably, Tesla is not among these companies. It holds a permit to test its technology in California, but only in vehicles with a driver. A total of 50 companies hold that permit according to the government website, thus we can say that holding this permit is “nothing special”. Many of Tesla’s peers, including Mercedes-Benz (OTCPK:MBGYY) and NIO (NIO), hold the same permit.

From a regulatory viewpoint, Alphabet’s offering in this space seems way more advantaged — it stands out among the dozens of companies that are active in self-driving tech, while Tesla seems to be in the middle of the pack. The same holds true when we look at commercialization.

While Tesla demands money from buyers of its tech even though that is only in beta testing, it is not allowed to commercialize it in a robo-taxi way. Waymo, on the other hand, has deployed its self-driving taxis in several cities including San Francisco, where riders can book rides via Alphabet’s apps.

Of course, there is no guarantee that Alphabet’s lead will hold. It is possible that Tesla eventually manages to hit a home run with its tech. But to me, it does not look like this is the most likely scenario — it seems more reasonable (to me) to assume that the current leaders with the most advantaged projects will continue to hold their leadership position in this space.

Both companies have seen their shares drop back this year, which means that their valuations have compressed. In other words, both stocks are cheaper today than they were at the beginning of the year, although that does not necessarily mean that they are cheap in absolute terms.

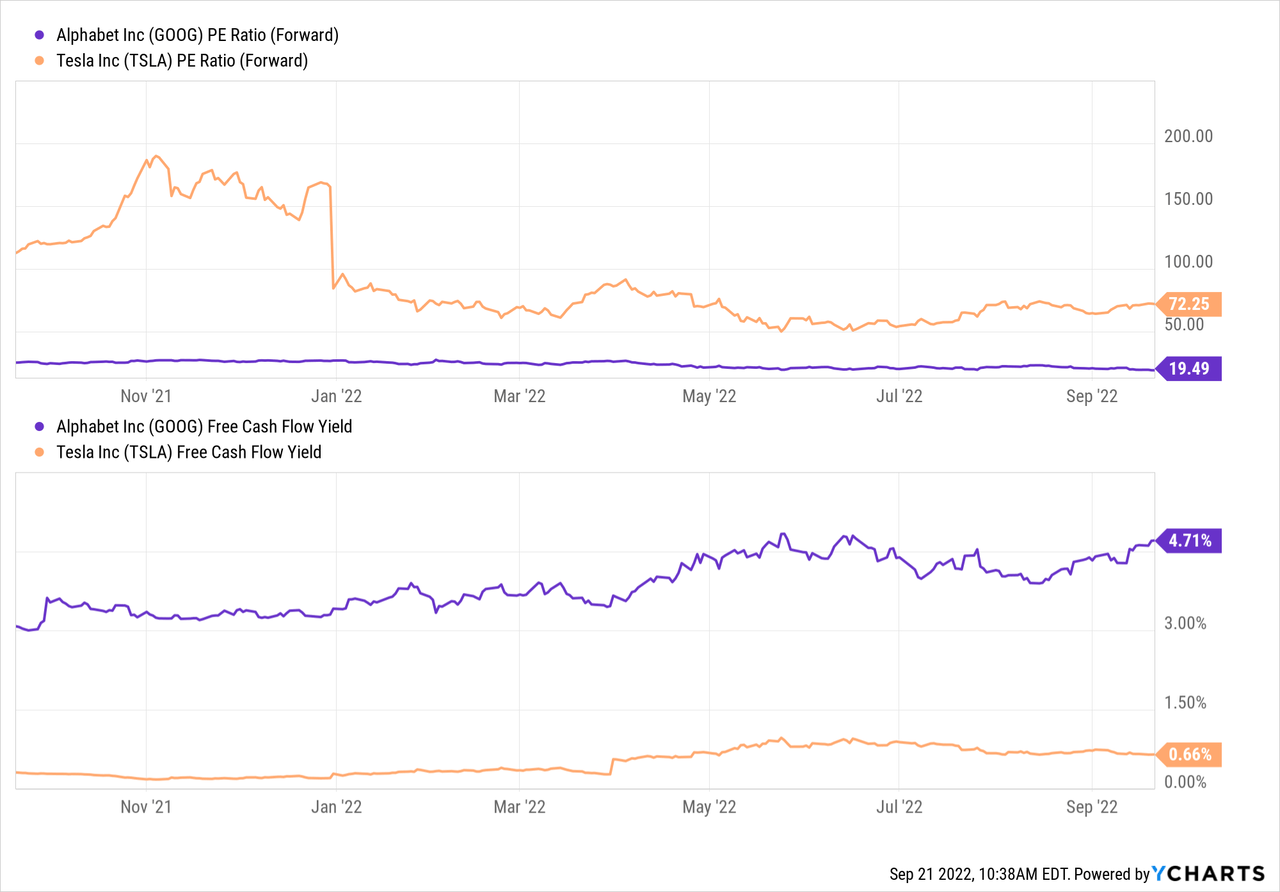

Looking at the earnings multiple for the current year, Alphabet seems quite inexpensive, while Tesla still trades at a premium valuation:

Alphabet is trading at less than 20x forward net profit, for an earnings yield of 5%. Tesla is trading at around 3.5x that valuation, as its earnings yield is in the 1.5% range as its earnings multiple still is north of 70. Of course, one can argue that free cash flows are even more important than net profits. After all, dividends and buybacks are financed with (free) cash, and debt reduction, acquisitions, etc. also depend on a company’s ability to throw off cash. In that regard, Alphabet looks even better relative to Tesla. Alphabet’s free cash flows are relatively comparable to its net profits, as the trailing free cash flow yield is in the 5% range as well.

The same does not hold true for Tesla, as its free cash flow yield of not even 0.7% is just half as high as its earnings yield. The big discrepancy can be explained by the capital-intense nature of the automobile industry. Factories need to be built and retooled regularly, the companies in this space need large amounts of working capital for unfinished products, raw materials, and so on. That’s why free cash generation generally is weak in the automobile space, thus this is not a Tesla-specific issue. Instead, Tesla is just performing in line with other automobile companies that have weak cash generation. Alphabet does not need to spend heavily on raw materials, factories, factory retooling, and so on. Its business model is much more shareholder-friendly as operations can be scaled up efficiently without large capital expenditure requirements — letting users stream one more video on YouTube or see one more ad on Google does not require any meaningful cash outlays on Alphabet’s side.

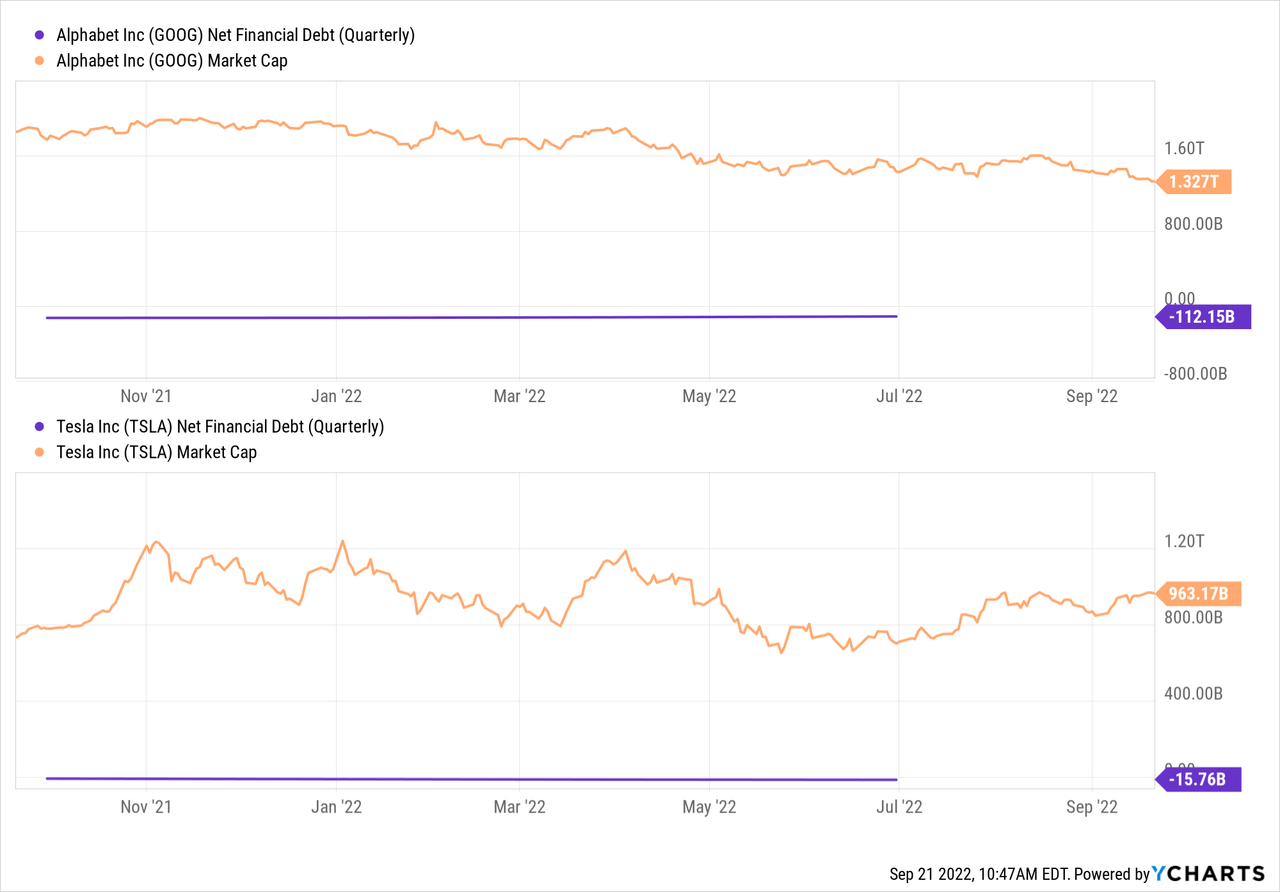

Not only does Alphabet look much cheaper than Tesla, but its way stronger free cash generation has also resulted in a way better balance sheet.

Tesla has a $16 billion net cash position, which is quite solid. But that’s less than 2% of Tesla’s market capitalization. Meanwhile, GOOG has a net cash position of $112 billion, which is 7x as much as what Tesla has, and which is equal to more than 8% of Alphabet’s market capitalization. Alphabet thus has much more financial firepower for shareholder returns, e.g. via buybacks, for acquisitions, and last but not least, its huge net cash position reduces risks considerably. In case we see a steep global economic downturn, Alphabet’s more than $100 billion in net cash insulates the company very well from financial troubles, while Tesla would be more exposed — not only is its cash “safety net” much smaller, but the automobile industry is also more cyclical and vulnerable to recessions relative to the software and communication services industries. In recent weeks we possibly got a glimpse of that, as delivery times for many of Tesla’s models declined to just a couple of weeks — that could be the result of increasing reluctance by consumers to spend heavily on a new vehicle in the current economic climate.

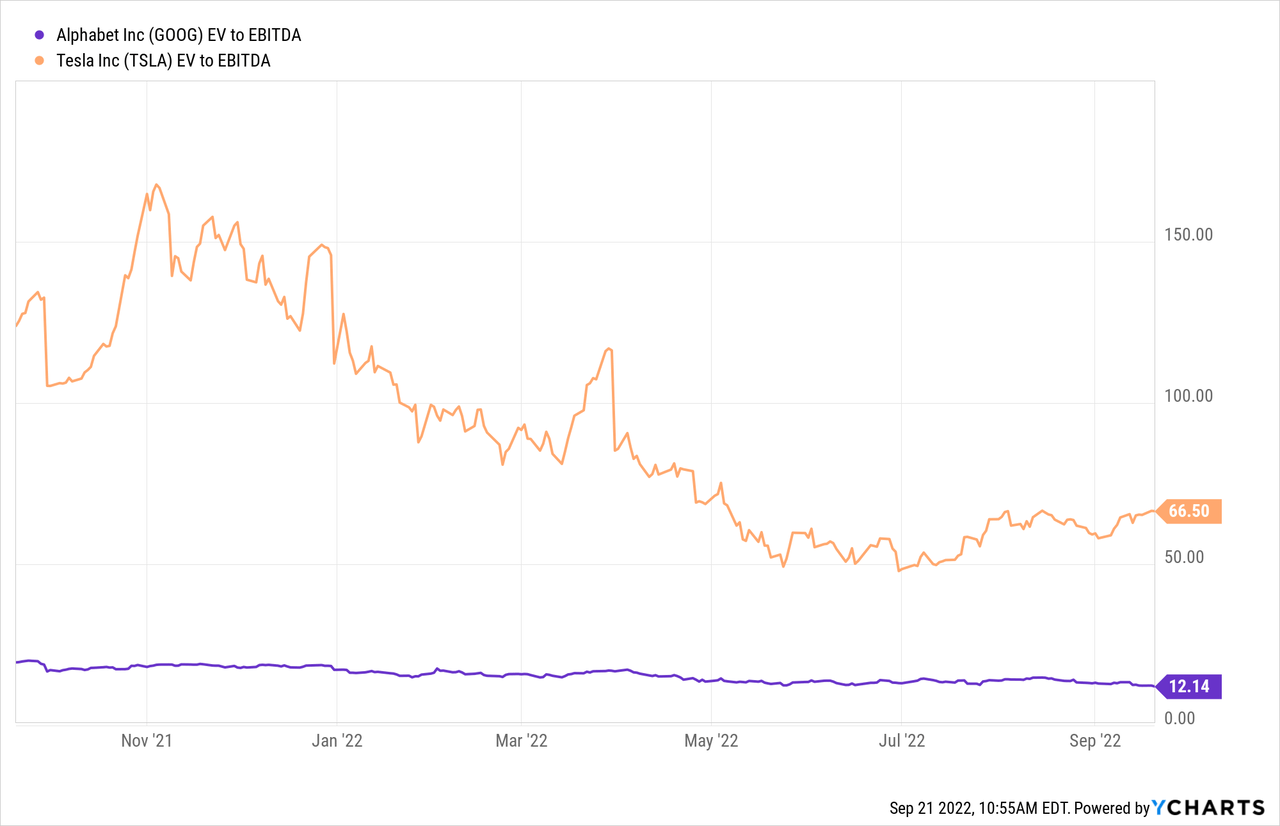

When we account for the net cash positions of both companies, Alphabet’s undemanding valuation drops to an even lower level:

At just 12x trailing EBITDA, Alphabet trades at a pretty undemanding valuation, especially when we account for its market leadership and healthy growth. Tesla is trading at 5x Alphabet’s EV/EBITDA multiple. It has pretty strong growth as well, at least in the past (see the aforementioned backlog decline and vulnerability to an economic downturn). But with its way weaker cash generation, lower margins, intensifying competitive pressures, and weaker self-driving tech, the current valuation does not seem attractive. One can argue that Tesla would be very attractive at a 12x EBITDA multiple, but at 5x the valuation of Alphabet, Alphabet looks like a significantly more compelling choice to me.

Some Tesla bulls mainly are in it for Tesla’s self-driving potential. I don’t think Tesla is in a leadership position here, but it is of course possible that the company becomes more successful over time. In case it manages to solve true self-driving anywhere before anyone else, that would result in a lot of earnings potential. But betting on that is not my investment style, and Tesla wouldn’t be my first choice even if I wanted to bet on any company solely for its autonomous driving tech.

The software/communication services industries offer great margins, strong free cash generation, and long-term growth potential. It also isn’t very cyclical. All these things hold true for Alphabet, and the company is an absolute leader in its space. The automobile industry as a whole is significantly less attractive, due to weak margins, high capital intensity, and so on. These things hold true for Tesla as well, even though it’s not a legacy automobile company. Tesla has a strong brand in the EV space, but competitive pressures are rising, and BYD (OTCPK:BYDDY) has overtaken it already in total EV sales (including plug-in hybrids). Due to these reasons, I believe that Alphabet is more suitable for a long-term investment. Since it is also way cheaper than Tesla while being one of just a few companies with self-driving cars deployed commercially, I favor it over Tesla.

Is This an Income Stream Which Induces Fear? The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

This article was written by

If you want to reach out, you can send a direct message here on Seeking Alpha, or an email to [email protected].

Disclosure:

I work together with Darren McCammon on his Marketplace Service Cash Flow Kingdown.

Disclosure: I/we have a beneficial long position in the shares of GOOG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.