blackCAT/E+ via Getty Images

Global-e (GLBE) has performed very strongly in its short time as a public company. The company has delivered strong growth even as it laps pandemic quarters, and it is easy to construct a bullish story on account of the e-commerce tailwinds. GLBE appears to operate in an important niche in enabling international e-commerce, which I predict will help it sustain elevated growth for the next decade and more. In this report, I analyze the valuation and explain how I think about the future of this stock.

GLBE went public on May 12th, 2021, pricing its initial public offering at $25 but closing barely higher at $25.50 per share. In spite of the hot IPO and tech market, that would have been an incredible time to buy, as GLBE has delivered triple digit returns in a matter of months.

The stock has since come back slightly amidst the weakness in the tech sector. Is it time to buy?

GLBE’s mission statement, as stated in its F-1, is to “make global e-commerce ‘border agnostic.’ In short, GLBE powers the international e-commerce experience. The reader is likely quite familiar with Amazon (AMZN) and the convenience that e-commerce has brought to the retail experience. But what if a shopper, located in Korea, wants to purchase a retail product from an American company? GLBE helps to make that possible.

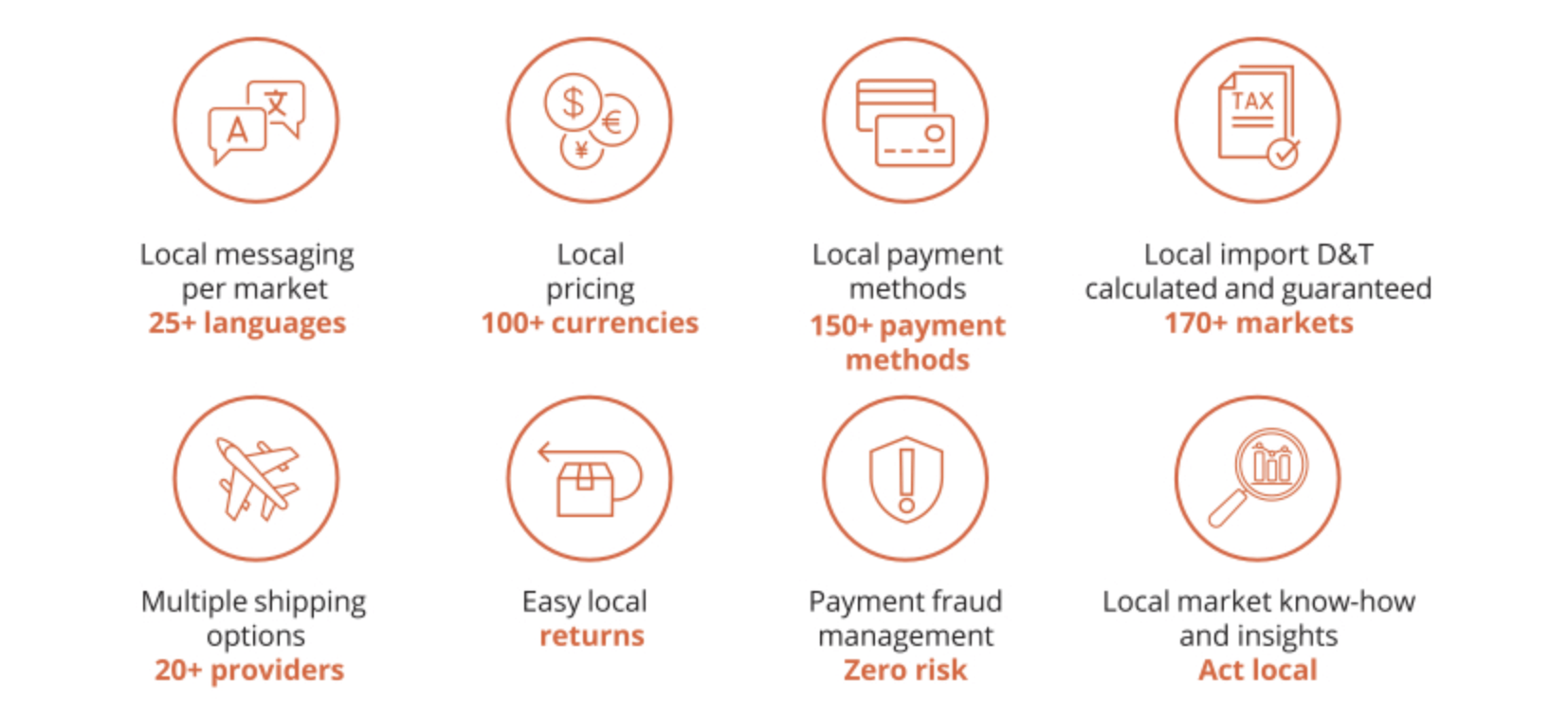

From the customer’s perspective, GLBE accepts over 150 local payment methods, provides translated versions of checkout experiences, and facilitates local returns.

(Global-e F-1)

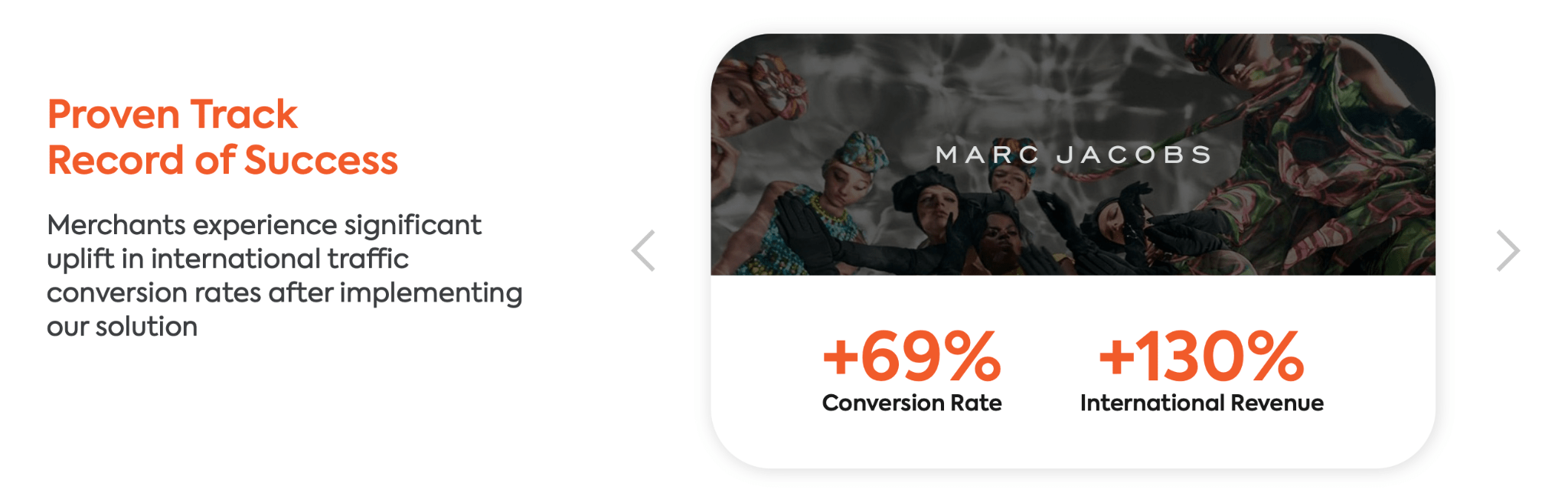

From the seller’s perspective, GLBE manages the finer details such as import duties and taxes in order to increase the target audience. GLBE estimates that its sellers experience an uplift of around 60% in international traffic conversion.

(Global-e)

In short, GLBE aims to make international e-commerce as convenient as domestic e-commerce. GLBE makes buying online a ubiquitous experience – regardless if the purchase is domestic or international.

GLBE has earned the trust of hundreds of retailers and brands.

(Global-e)

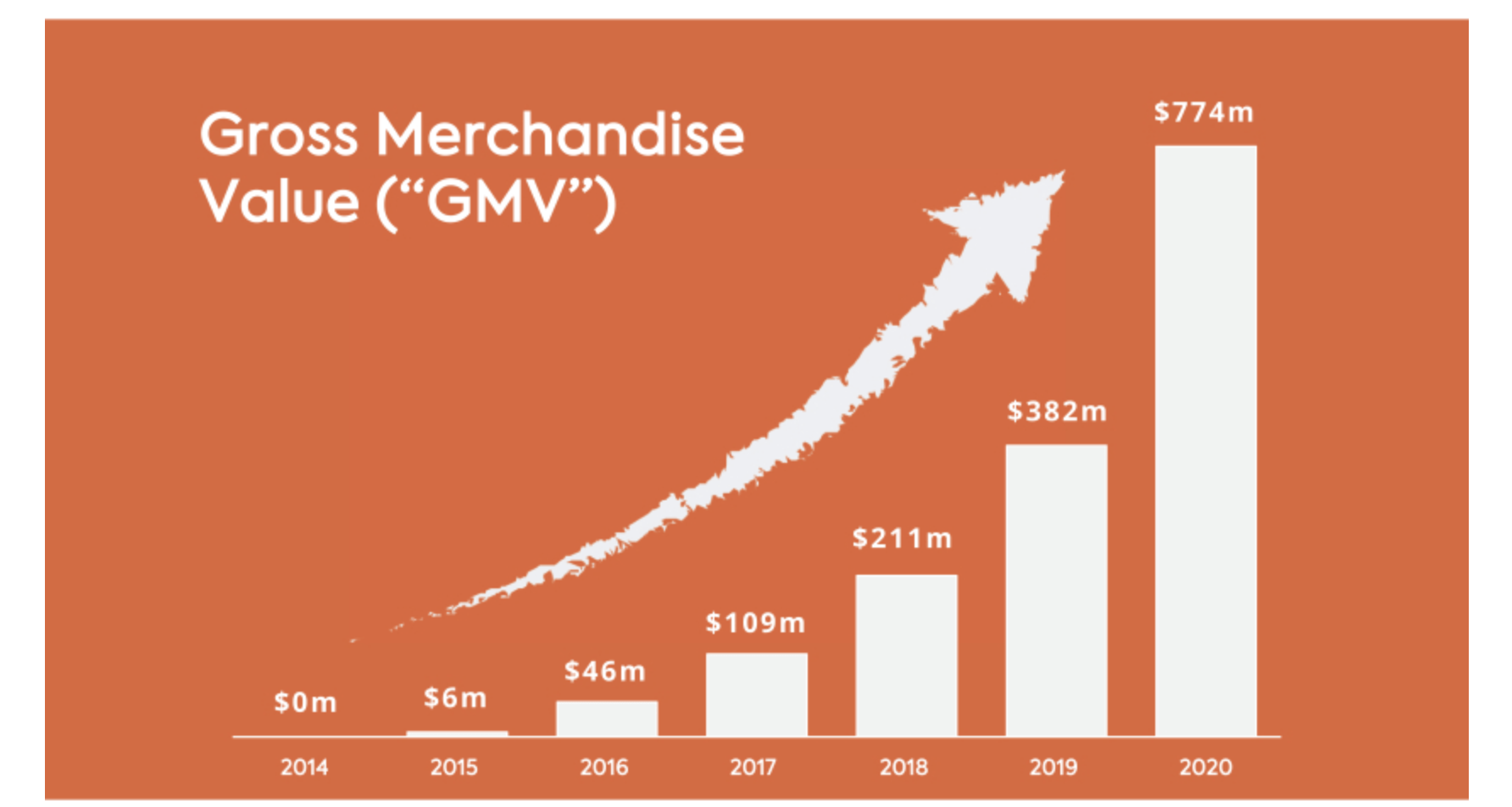

Given the high improvement in international conversion rates, it isn’t surprising that GLBE has seen accelerating growth in gross merchandise value (‘GMV’).

(Global-e F-1)

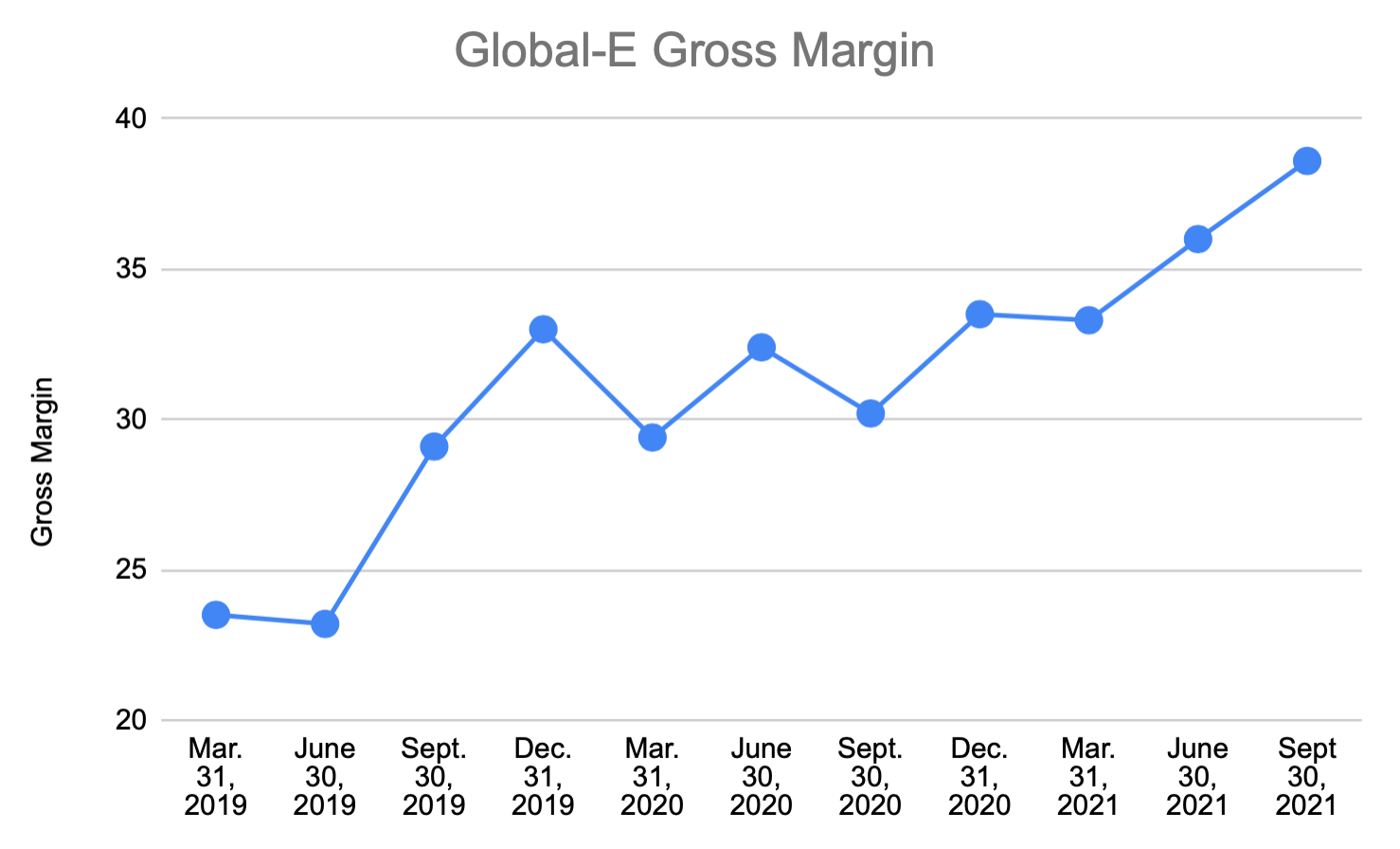

GLBE earns revenues in two categories: service fees and fulfillment revenues. While that might scare off investors due to potential for low margins, it is worth noting that gross margins have been improving quickly in recent quarters and recently hovered around 38%:

(Chart by Author, data from F-1)

How do customers find GLBE? Just prior to the IPO last year, Shopify (SHOP) took a $193 million stake in the company that gave it 7.75 million shares and warrants worth up to 11.85 million in shares. In return, GLBE is now offered as an international e-commerce plugin for Shopify sellers. This partnership should help power future growth.

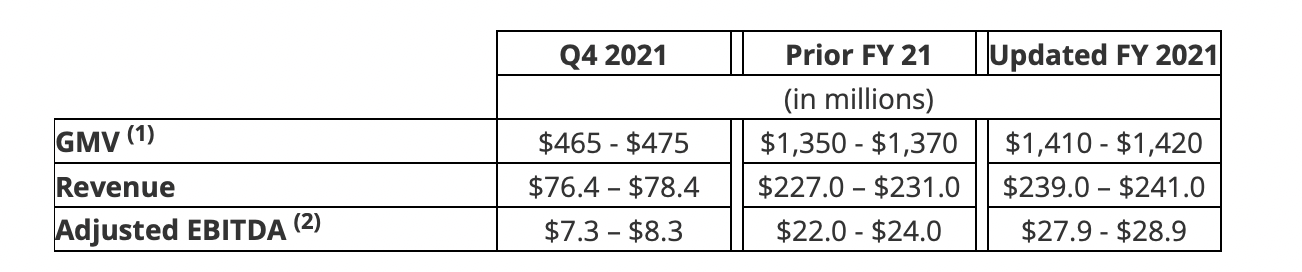

In its latest quarter, GLBE grew revenues by 77% to $59.1 million with adjusted EBITDA of $7.7 million. GLBE also raised full-year revenue guidance by around 5% to $240 million at the midpoint. This was after the 9% raise in the prior quarter.

(2021 Q3 Earnings Release)

The strong growth rate is one thing, but I expect the company to deliver sustained growth due to the strong secular tailwinds from both international e-commerce and e-commerce itself.

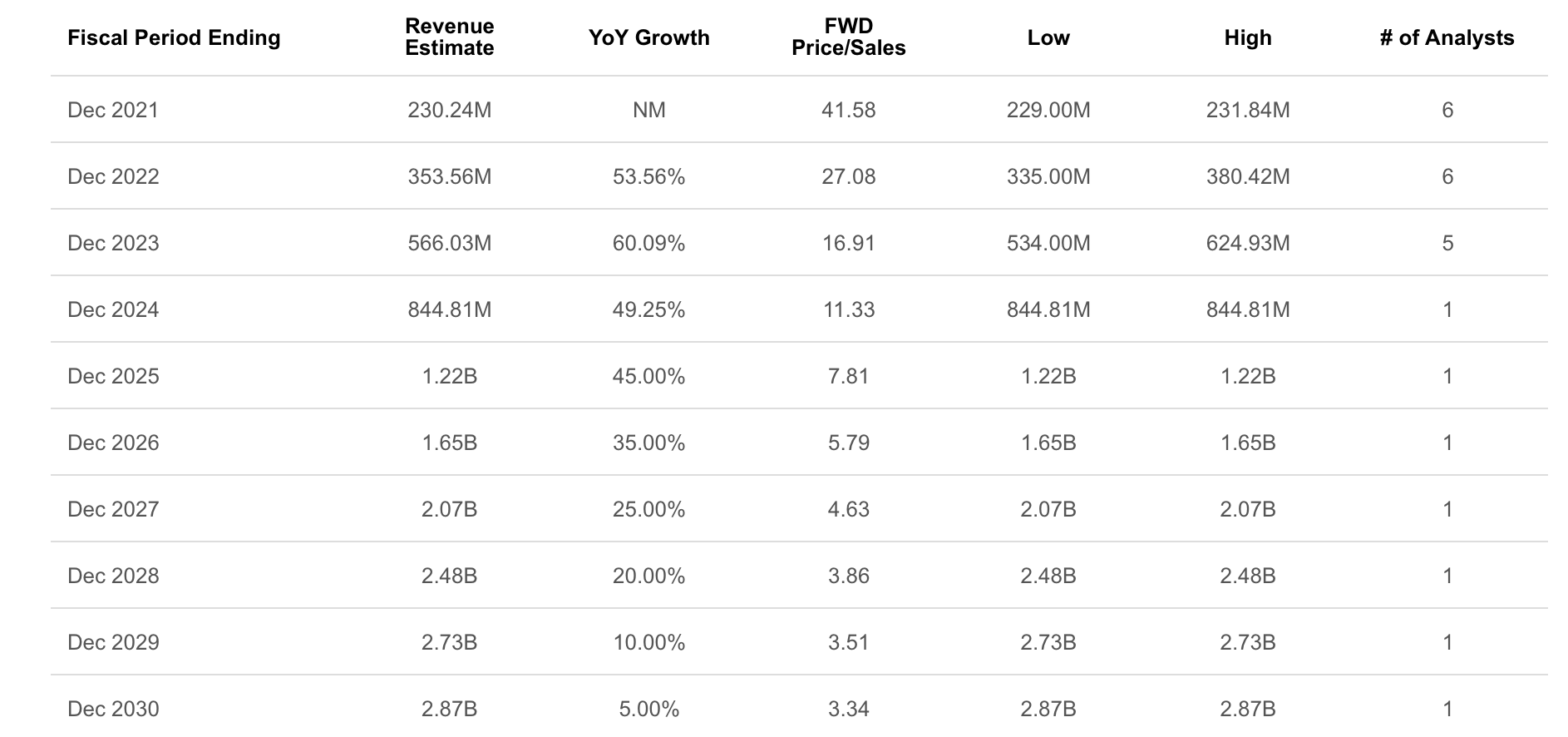

There’s an attractive growth story at play, but has the valuation gotten stretched after the run-up? That may be true. GLBE is trading at around 42x trailing sales. Yet, as discussed earlier, gross margins are low at 38% and as a result, I find it more appropriate to value the stock on the basis of gross profits in order to normalize for margins. GLBE is trading at 104x trailing gross profits, which obviously isn’t cheap in light of the 128% trailing growth rate. That said, 2020 and 2021 showed that the market is willing to price in many years of growth, and GLBE’s multiple should improve quickly with such a rapid growth rate. Let’s take a look at consensus estimates below.

(Seeking Alpha)

Wall Street expects GLBE to grow its revenues such that it would be trading at around 11x 2024e revenues. Assuming stable gross margins, that would equate to 31x gross profits. In all honesty, that multiple doesn’t look that cheap as compared with the 49% estimated growth in 2024 – and that’s more than three years from now. Yet the real opportunity comes from its potential ability to sustain rapid growth rates. Just look at how SHOP was able to sustain elevated growth year after year, in clear defiance of the law of large numbers.

Chamath Palihapitiya has written about the beauty of “slow compounding.” The idea is that slow growth rates persisted over long periods of time is more valuable than high growth rates sustained over short periods of time. In this case, I’d expect GLBE to sustain 15% to 20% annual growth for many years after 2024, and I expect that this principle is driving the elevated valuation being assigned to the stock.

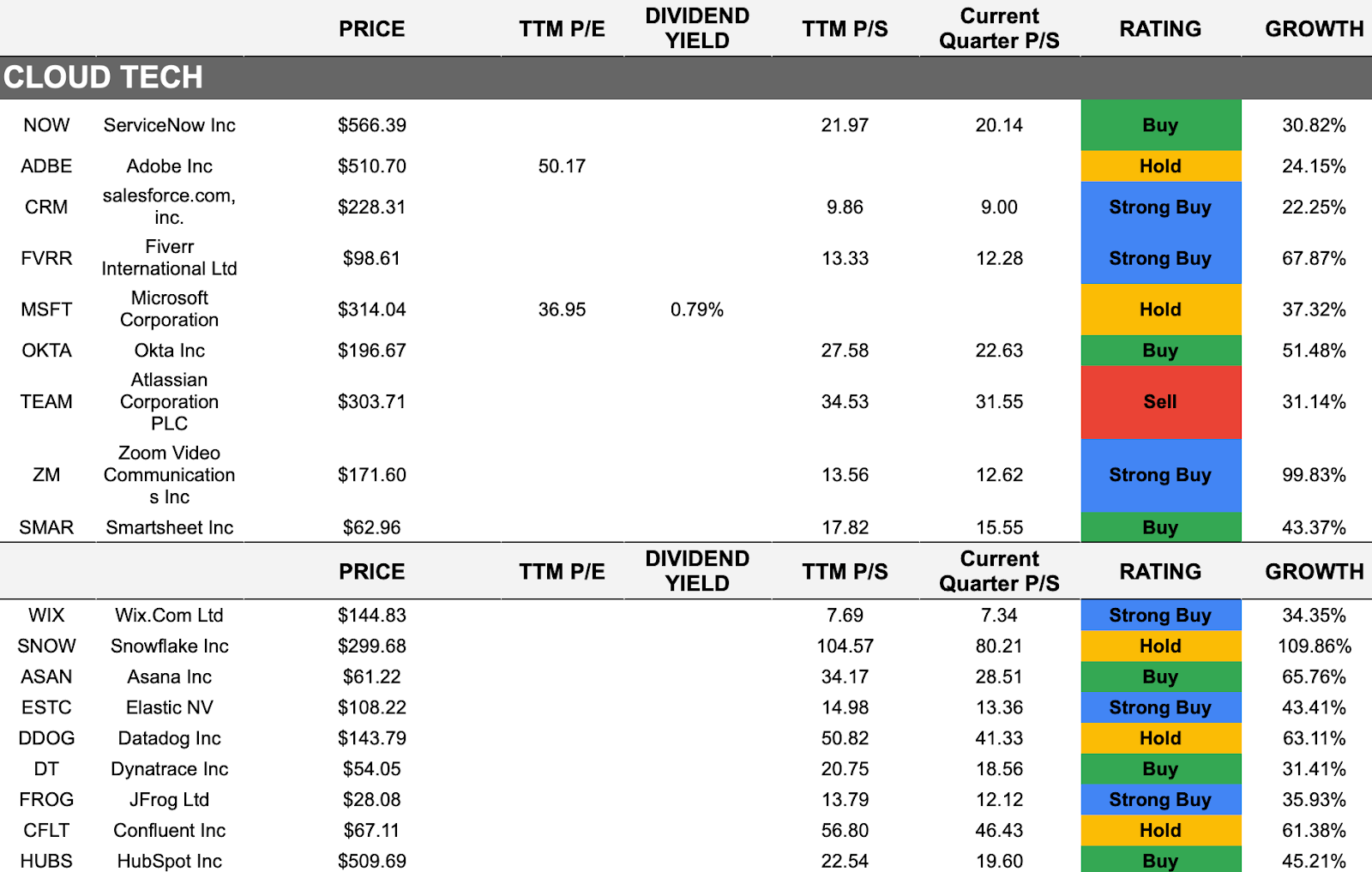

This leads me to reason that GLBE should deliver positive or even market-beating returns over very long holding periods. However, Wall Street consensus estimates do not appear obviously understated, at least over the next 5-7 years, and the stock does not appear obviously undervalued even based on the generous estimates. This kind of setup does not provide the asymmetric risk-reward opportunities that I typically look to provide subscribers. What’s more, we can see that many tech stocks in my coverage universe are flashing buy signals.

(Best of Breed Universe Watchlist)

Of the 80+ tech companies that I cover, approximately 90% are rated with a “buy” rating – that’s what happens after prices fall so quickly in a short amount of time. While GLBE may look buyable here, the premium valuation means that the stock might not be attractive relative to other stocks in the tech sector. The valuation reset among growth stocks has afforded investors the rare luxury of being able to filter on quality while being picky on price. While I could see myself buying GLBE in the future, I expect the biggest winners to come elsewhere in the sector.

For more coverage of undervalued growth stocks, including my top picks, consider subscribing to Best of Breed.

My portfolio is made up of a short list of stocks that I think will absolutely crush the market over the next decade.

Get access to my highest conviction ideas.

This article was written by

I run Best Of Breed, a research service uncovering high conviction ideas in the winners of tomorrow. I am ranked in the top 1% for financial performance on Tipranks.

Get access to my highest conviction ideas here.

Disclosure: I/we have a beneficial long position in the shares of AMZN, SHOP either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am long all holdings in the Best of Breed portfolio.