Justin Sullivan/Getty Images News

Justin Sullivan/Getty Images News

According to Seeking Alpha data (Wall Street price target), Tesla (NASDAQ:TSLA) has a low price target of $250, an average price target of $1003, and a high price target of $1620. Which price target is reliable? Some say that despite the astonishing performance of the company, the stock is overvalued. Some believe that due to the company’s Robotaxi plan and the EV market outlook, TSLA is undervalued. I am bullish on Tesla stock based on my estimations of the company’s 2022 revenues, adjusted EBITDA, my stock valuations using two different methods, and different scenarios. TSLA is worth between $1200 to $1300 per share.

In 2017, with about 103181 electric vehicles delivered by Tesla, the company’s EV sales to global EV stock ratio was about 2.8%. This ratio increased to 4.4% in 2020 and 6.1% in 2021. Due to the decreasing usage costs of EVs compared to gas cars, governments’ regulatory credits to push automakers toward producing more EVs, and environmental regulations, global EV stock will increase significantly in the following years. Is Tesla able to maintain its EV sales to EV stock ratio or even increase it? The company’s expenditure on R&D has increased in recent quarters (Cybertruck, Tesla Semi, and Roadster are in development), making it able to introduce new models. Also, Tesla has been able to increase its efficiency in recent quarters. Tesla’s cost of sales to total revenues ratio decreased from 79% in 1Q 2021 to 71% in 1Q 2022. Finally, Tesla’s increasing free cash flow will help the company to answer to the EV demand. Tesla’s free cash flow (TTM) increased from $1103 million in 1Q 2020 to $3974 million and $6950 million in 1Q 2021 and 1Q 2022, respectively.

On the other hand, Tesla’s competitors are becoming stronger in the EV market. In terms of all-electric car sales market share, SAIC, Volkswagen, and BYD are Tesla’s biggest competitors. In 2021, Tesla’s market share was 21%, compared to SAIC, Volkswagen AG (OTCPK:VWAGY), and BYD’s (OTCPK:BYDDF) market share of 13%, 10%, and 7%. In 2021, Volkswagen delivered 93000 EVs in China, four times more than in 2020. Also, in 2021, Volkswagen was the market leader for EVs in Europe with a market share of 25%. However, due to the reasons I mentioned, Tesla will be the most competitive EV maker in the following years.

In its 1Q 2022 financial results, Tesla reported 1Q 2022 automotive revenues and total revenues of $16861 million (up 87% YoY) and $18756 million (up 81% YoY), respectively. Tesla’s 1Q 2022 81% revenue growth was driven by higher average selling price (ASP), increased vehicle deliveries, and growth in other parts of the business. The company’s 1Q 2022 automotive and total gross margin increased by 636 bps and 779 bps to 32.9% and 29.1%, respectively. Tesla reported 1Q 2022 operating expenses of $1857 million, compared with 1Q 2021 operating expenses of $1621 million. The company reported 1Q 2022 adjusted EBITDA and 1Q 2022 adjusted EBITDA margin of $5023 million (up 173% YoY) and 26.8% (up 906 bps YoY), respectively.

Tesla reported 1Q 2022 GAAP EPS of $2.86, compared with 1Q 2021 diluted GAAP EPS of $0.39, up 633%. This increase in the company’s EPS was due to increased vehicle deliveries, increased ASP, reduced COGS per vehicle despite inflationary pressures, an increase in regulatory credit sales, and lower stock-based compensation expense. However, operating expenses, raw material prices, and logistics costs increased in the first quarter of 2022. The company’s free cash flow increased from $239 million in 1Q 2021 to $2228 million in 1Q 2022. Moreover, Tesla’s capital expenditure increased from $1348 million in 1Q 2021 to $1767 million in 1Q 2022, up 31%. Furthermore, in the first quarter of 2022, Tesla repaid $2.1 billion of its debt, decreasing its total debt (excluding vehicle and energy product financing) to below $100 million.

According to Global EV Outlook 2021, automakers have committed to increasing their electric vehicle production (see Figure 1). In 2021, Ford (F) was expected to offer 40 new EV models by the end of 2022, and BMW Group (OTCPK:BMWYY) was expected to offer 25 new EV models by 2023 (Global EV Outlook 2022 will be published on 23 May 2022). Figure 1 shows that by 2030, automakers will shift significantly to electric vehicles. Is it dangerous for Tesla’s market share?

Figure 1 – Automakers commitment to produce electric vehicles

Global EV Outlook 2021

Global EV Outlook 2021

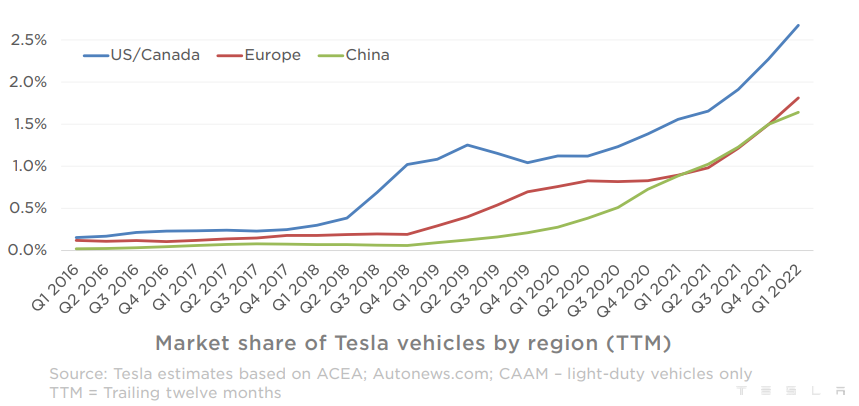

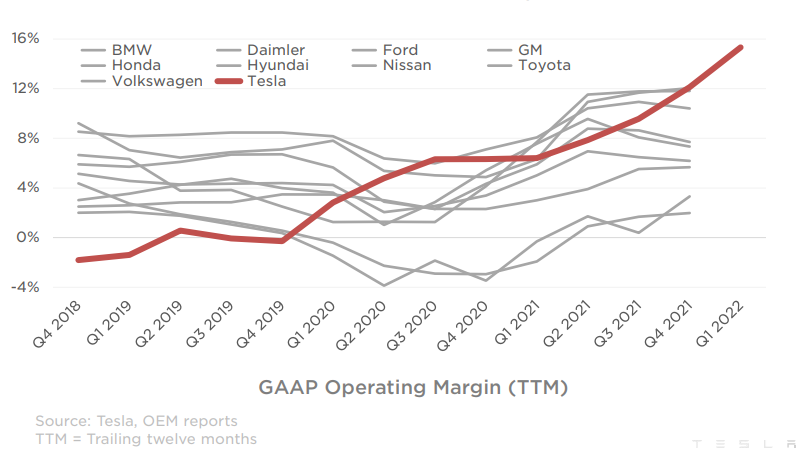

Figure 2 shows that from 1Q 2016 to 1Q 2022, Tesla’s market share has been increased in all the regions. Figure 3 shows that in 4Q 2018, Tesla’s operating margin was lower than its competitors. However, by the end of 2021, Tesla’s operating margin bypassed its competitors’ operating margins.

Figure 2 – Market share of Tesla vehicles by region

Tesla 1Q 2022 financial report

Tesla 1Q 2022 financial report

Figure 3 – Automakers’ operating margin (TTM)

Tesla 1Q 2022 financial report

Tesla 1Q 2022 financial report

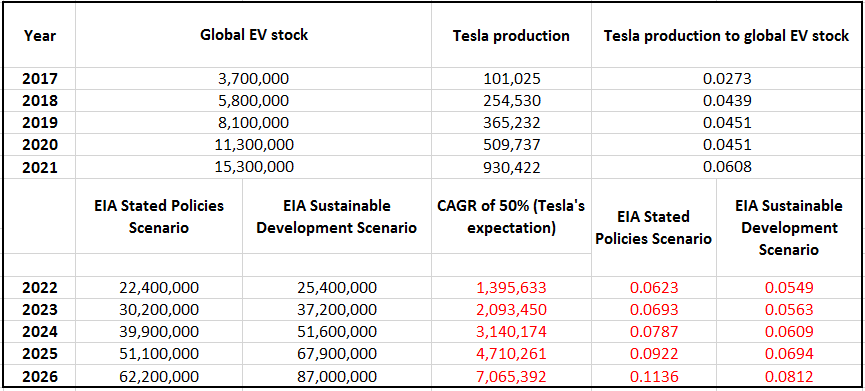

Table 1 shows that with a CAGR of 33%, the global EV stock has increased from 3.7 million in 2017 to 15.3 million in 2021. During this period, Tesla’s production has increased from 101025 in 2017 to 930422 in 2021 (with a CAGR of 56%). Thus, Tesla’s production to global EV stock ratio increased from 0.03 in 2017 to 0.06 in 2021. According to the Global EV Outlook 2021, global EV stock will increase to 62 million (based on EIA Stated Policies Scenario) and 87 million (based on Sustainable Development Scenario). On the other hand, Tesla expects its production to increase with a CAGR of 50% in the next five years. Can we rely on these expectations? I have three reasons to expect Tesla production to increase by an average annual growth rate of even more than 50% in the next five years:

1- The cost of charging an electric car is much lower than fueling a gas car. According to a study by the University of Michigan, an EV costs $485 per year. On the other hand, the average cost to use a gas car is about $1117 per year. Tesla cars cost between 3 to 5 cents per mile. Now, the national average for gasoline per gallon is more than $4.3, and in the United States, gas cars go between 11 miles to 51 miles per gallon. Thus, in the United States, gas cars cost between 8 cents to 39 cents per mile.

2- To reduce carbon emissions, governments give credits to automakers that produce environmentally friendly cars. Companies that only build EVs can sell their regulatory credits to other automakers. In the first quarter of 2021, Tesla sold $518 million worth of regulatory credits, making the company able to report a profit. In 1Q 2022, Tesla sold $679 million worth of regulatory credits, 20% of its net income. Tesla’s regulatory credits increased by 31% YoY in 1Q 2022. Meanwhile, it is worth noting that since 2Q 2021, Tesla does not need regulatory credits to report a profit in its quarterly reports. Regulatory credits are great incentives to push automakers toward producing EVs.

3- In the United States, under Biden’s order, the government plans to end petrol car purchases by 2035 to reduce carbon emissions. Also, China plans to ban the sales of fossil-fueled cars by 3035. Moreover, European Parliament’s environmental committee plans to ban selling new fossil-fueled cars in most parts of the EU. Besides carbon emission considerations, you should know that EVs are more efficient than gas cars. “EVs convert over 77 percent of the electrical energy from the grid to power at the wheels. Conventional gasoline vehicles only convert about 12 percent – 30 percent of the energy stored in gasoline to power at the wheels,” the US Department of Energy reported.

Thus, I believe that Tesla’s expectation about its production is reliable. I expect that by 2026, Tesla’s production to global EV stock ratio will increase to 0.11 and 0.08, based on EIA’s Stated Policies Scenario and Sustainable Development Scenario, respectively. Tesla will perform stronger than before, and its market share is not in danger.

Table 1 – Tesla production to global EV stock ratio

Author

Author

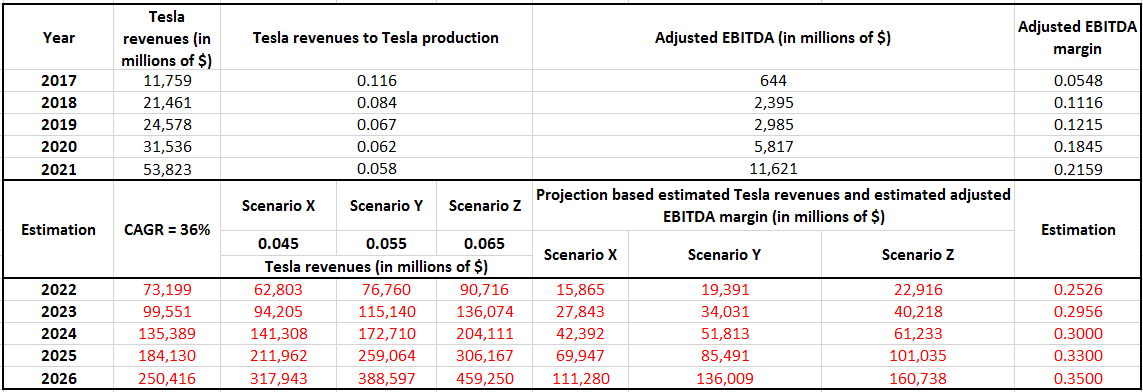

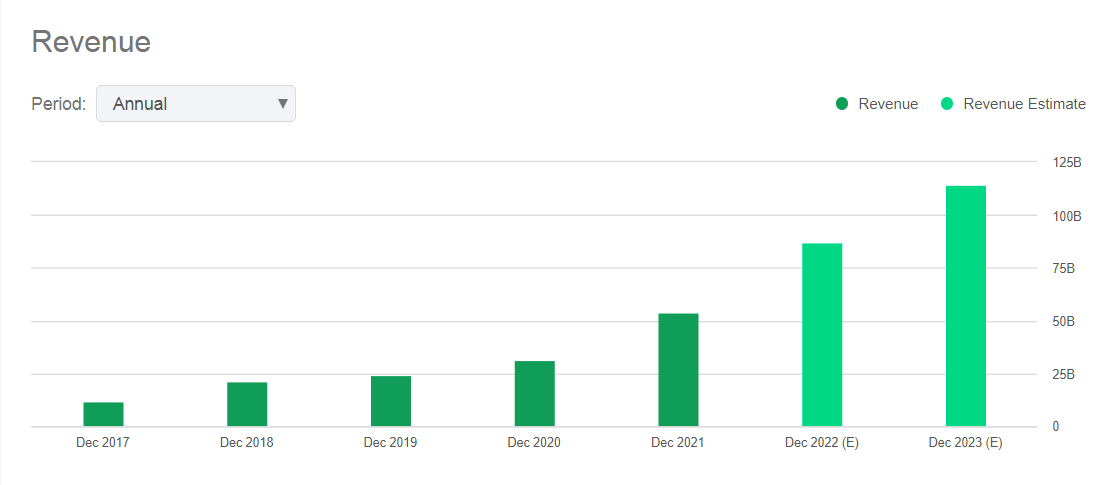

Using estimated Tesla production from 2022 to 2026, I predict the company’s revenues based on three scenarios from 2022 to 2026. Based on Scenario Y (revenues to production ratio of 0.055), I estimate 2022 revenues of $76760 million for Tesla, compared with 2021 revenues of $53823 million. Also, based on Scenario Z (revenues to production ratio of 0.065), I estimate 2022 revenues of $90716 million for Tesla. According to Seeking Alpha’s revenue estimate, Tesla is expected to report a 2022 revenue of $87 billion (see Figure 4). Moreover, I estimate Tesla’s adjusted EBITDA from 2022 to 2026. Based on Scenario Y and an adjusted EBITDA margin of 0.25 in 2022, I estimate a 2022 adjusted EBITDA of $22916 million for Tesla. I will use my estimations of Tesla’s adjusted EBITDA in the valuation section.

Table 2 – Estimation of Tesla revenues, adjusted EBITDA, and adjusted EBITDA margin

Author

Author

Figure 4 – Tesla revenue estimate

Seeking Alpha

Seeking Alpha

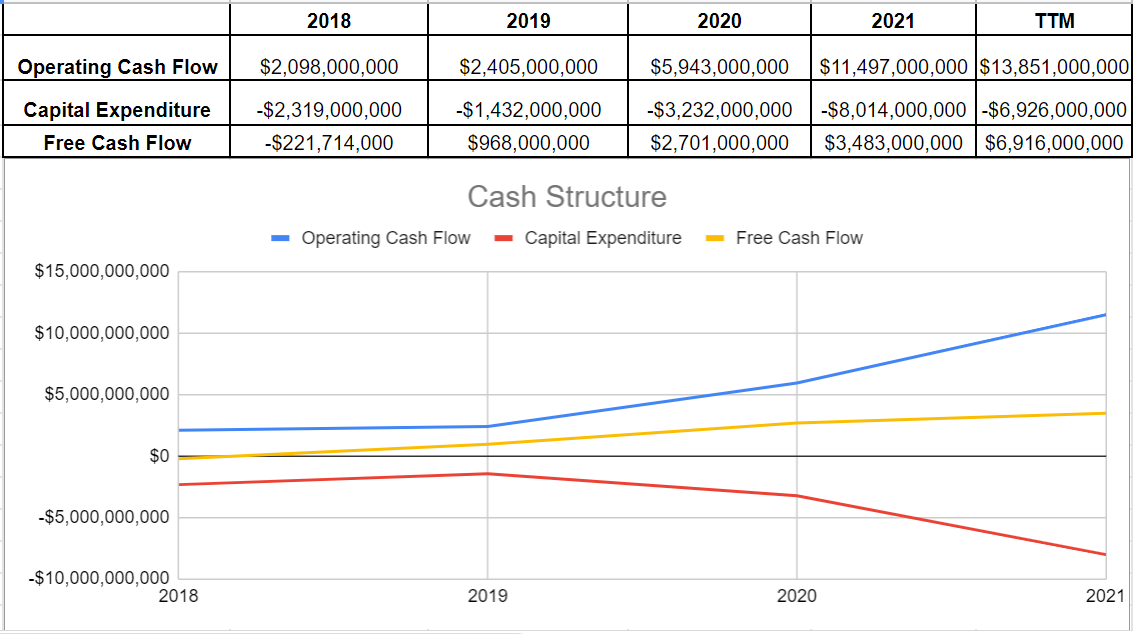

Thanks to the strong operating conditions during the last couple of years. TSLA’s cash flow performance recovered from the downturn of 2020, with its operating cash flow surging to $11.49 billion in 2021 and $13.85 billion (TTM), respectively. Thus, TSLA’s operating cash flow has grown by more than double its level of only $5.94 billion at the end of 2020. On the other hand, the company’s capital expenditure increased by 147% to $8 billion at the end of 2021, which could be a sign of encouraging growth and boosting productivity. Ultimately, TSLA’s TTM free cash flow has been boosted impressively to $6.91 billion from its level of $968 million before the COVID-19 pandemic started at the end of 2019 (see Figure 5).

Figure 5- Tesla’s cash structure

Author

Author

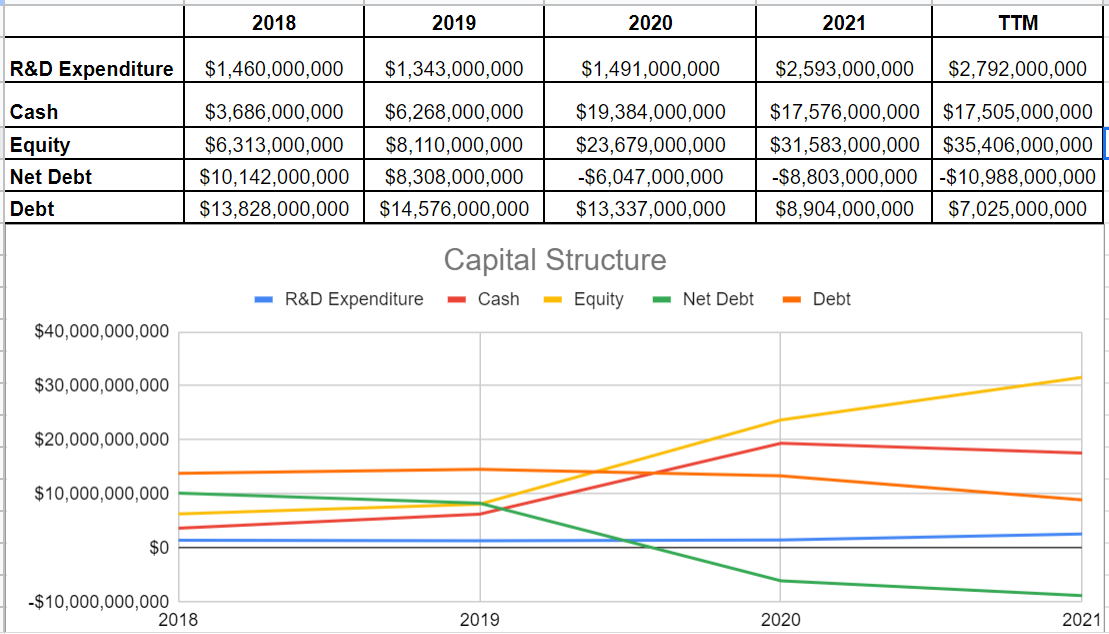

In Tesla’s capital structure, we can observe that the company’s cash balance surged impressively to $19.38 billion in 2020 versus its level of $6.26 billion at the end of 2019, then edged down to $17.57 billion by the end of 2021. Meanwhile, 2021 also saw TSLA’s net debt shrink to $(8.8) billion from its previous level of $(6.04) billion. Also, TSLA’s debt amount dropped severely to $8.9 billion in 2021 from its level of $13.3 billion at the end of 2020. Meanwhile, the company’s equity level surged amazingly by 33% to $31.5 billion at the end of 2021 (see Figure 6).

Figure 6- Tesla’s capital structure

Author

Author

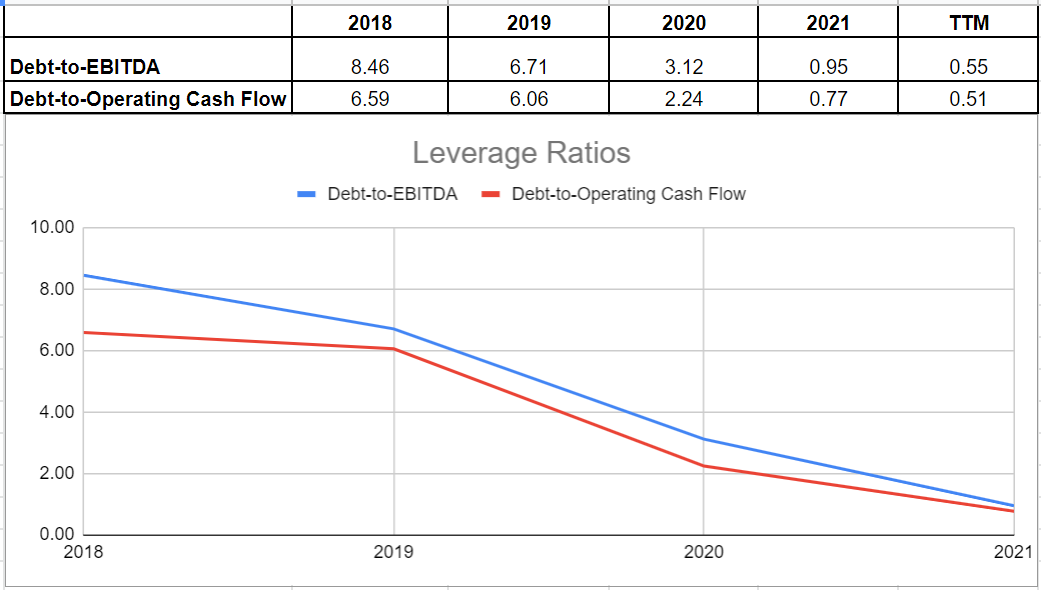

Following TSLA’s strong cash balance and decreasing debt during 2021, it is not surprising to see improvements in its leverage position . TSLA’s leverage decline has resulted in its TTM debt-to-EBITDA and TTM debt-to-operating cash flow ratios, which have declined to 0.55 and 0.51, respectively. Both of these amounts are well beneath the amount of 6.71 and 6.06, respectively, at the end of 2019 before the COVID-19 pandemic (see Figure 7).

Figure 7- TSLA’s leverage ratios

Author

Author

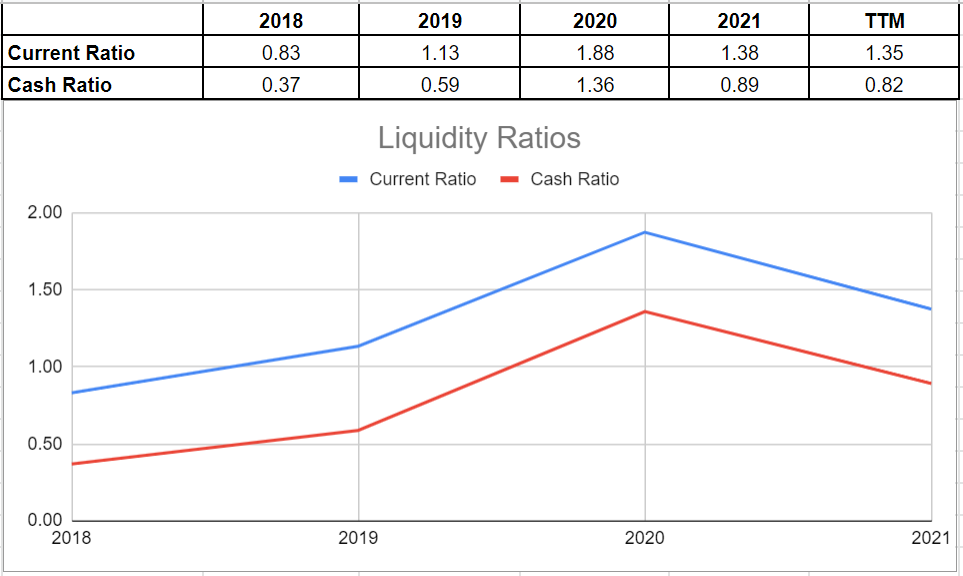

Following the company’s cash balance edging down during 2021, its liquidity ratios declined slightly at the end of 2021. However, thankfully the liquidity condition is still strong, with a TTM current ratio of 1.35 and a TTM cash ratio of 0.82. Also, the operating conditions are currently in a good position, which provides safe fiscal stability. Looking ahead, TSLA’s well-performed operations and increasing free cash flow will help the company to increase its liquidity at the end of 2022 (see Figure 8).

Figure 8- Tesla’s liquidity ratios

Author

Author

Based on Wall Street analysts’ ratings, Tesla stock has a price target of between $250 to $1620 (see Figure 9). It is a wide range, isn’t it? With a price target of $250, TSLA is a strong sell, and with a price target of $1620, the stock is a strong buy. Figure 2 shows that among mega-cap stocks when it comes to Tesla, there is controversy among analysts. We can see analysts’ mixed ratings on TSLA during the last three years. On the other hand, analysts have a consensus buy/strong buy ratings on other mega-cap stocks.

Figure 9 – Tesla stock price target

Seeking Alpha

Seeking Alpha

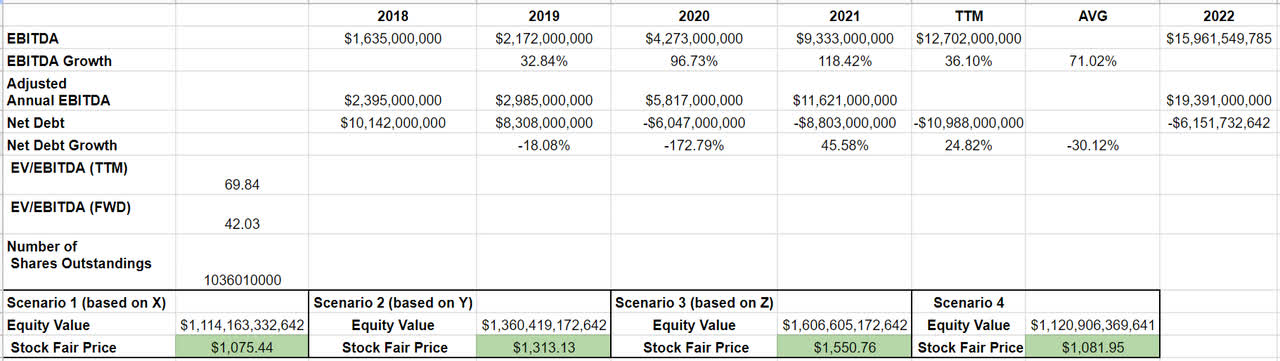

Regarding TSLA stock valuation, I used a couple of valuation methods. I noticed that both are in the same line and indicate that the stock is undervalued. To estimate TSLA’s fair value, I investigated its EBITDA growth during the last years. The company’s EBITDA grew impressively, about 70% in recent years. Also, its net debt has declined by 30%, on average. As I mentioned earlier, there are different estimations regarding the company’s adjusted EBITDA in 2022. Based on these estimations, I investigated different scenarios for TSLA stock price (see Table 3).

Table 3 – Tesla stock valuation

Author

Author

Scenario 1: Based on scenario X, in which I estimate $15.86 billion for TSLA’s adjusted EBITDA in 2022, I evaluate that TSLA’s fair price is around $1075 per share, which shows a 34% upside potential.

Scenario 2: Based on Scenario Y, the company’s adjusted EBITDA will be about $19.40 billion at the end of 2022. So its price will have the upside potential to reach around $1313 per share.

Scenario 3: In scenario Z, I indicate that TSLA’s adjusted EBITDA will reach $22.9 billion in 2022. Therefore, the stock’s fair value would be $1550.7.

Scenario 4: If TSLA’s EBITDA grows by 70%, the company’s fair value will be about $1082 per share.

In a nutshell, I estimate that according to different scenarios, Tesla stock still has upside potential. Also, I believe that the second scenario is the most probable one based on TSLA’s financial statements. Thus, the stock has about 64% upside potential to reach $1,313.

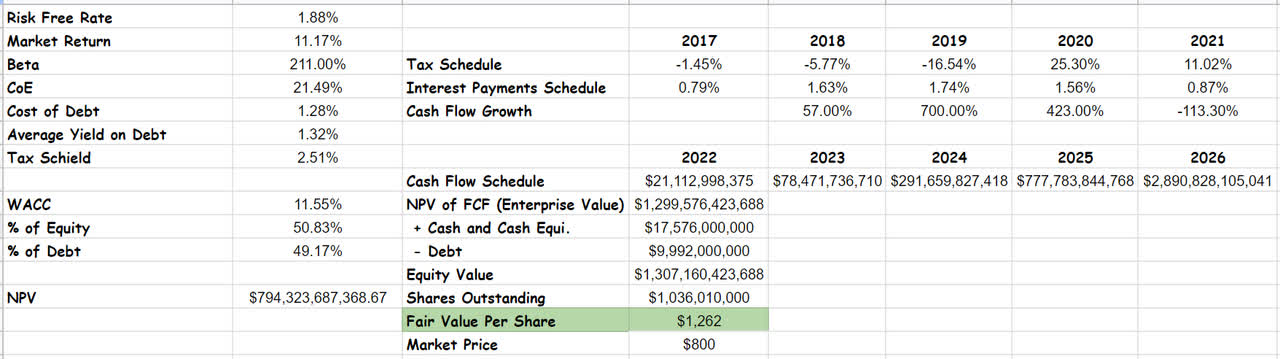

Besides, I use the DCF model to investigate Tesla’s intrinsic value and estimate its fair price per share. In spite of being a bit conservative, the DCF model is extremely detailed and does not require any comparable companies. As Table 4 represents, the DCF model determines a fair value of $1.3 billion for Tesla, and thus, it is $1262 per share.

Table 4- Tesla stock valuation based on DCF model

Author

Author

You may ask how I selected the most probable scenario in my first valuation method and how I estimated future free cash flows in the DCF model. In both valuation methods, Tesla’s revenues to production ratio and adjusted EBITDA are the main elements of my valuation. In the first valuation method, I said the second scenario is the most probable. I used an estimated 2022 adjusted EBITDA of $19391 million and a 2022 revenue to production ratio of 5.5%. Also, in the DCF model, I used the same numbers to estimate Tesla’s future free cash flows. Why? Tesla’s revenues to production ratio increased from %11.6 in 2017 to 5.8% in 2021. The company’s total production is increasing more than any metric in its financial statement. Thus, I believe Tesla’s revenues to production ratio keeps decreasing in the following years. With a CAGR of -13%, the most probable scenario for Tesla’s revenues to production ratio in 2022 is 5.5%. Also, the company’s adjusted EBITDA margin increased from 5.48% in 2017 to 21.59% in 2021. With a CAGR of 17%, the adjusted EBITDA margin of 25.26% in 2022, has the highest probability. I used the adjusted EBITDA margin of 25% to estimate a 2022 adjusted EBITDA of $19391 million for Tesla.

Based on the Global EV Outlook 2021, automakers have committed to increasing their electric vehicle production. However, from 1Q 2016 to 1Q 2022, Tesla’s market share has been increased in all the regions. Thus, it will not put TSLA’s market share in a danger. Also, TSLA’s strong cash balance and decreasing debt during 2021, provide improvements in its leverage position. Looking ahead, TSLA’s well-performed operations and increasing free cash flow will help the company to increase its liquidity at the end of 2022. Moreover, based on my estimations, TSLA’s adjusted EBITDA will be increased impressively at the end of 2022. In a word, I am bullish on TSLA stock since I estimate that the stock has a potential to reach between $1200-1300.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.